What, no Dijon?

Attribution: Mike Ganon

Why bother with marketing spin? He didn’t.

Scott Morrison doesn’t seem to have many veils left on when it comes to his view on China.

Last week he managed to piss off both China and France with his (light on detail) sub deal.

Reminds me of the Don’s Phase One trade deal – remember that? Don’t worry, no one else does, so here’s a refresher.

And our jigsaw puzzle playing PM also set a lot of tongues wagging with his long range Tomahawk missile plans.

Ker plunk!

This game won’t solve anything because in the event of a military war (as opposed to a trade/currency/technology/beef/wine/iron ore war), our neighbour outnumbers U.S. forces and also has the advantage of regional proximity to our fair island and surrounding strategic interests.

Why is this happening now? Is the timing, which comes just after the Afghan withdrawal, a premeditated yet thinly veiled retargeting of China by U.S.S. Mercantile?

Maybe. But at least on thing’s pretty clear.

The U.S. is worried.

The extent to which the U.S. is worried has been front and centre since the early days of the big and not so beautiful Trump administration.

The Don shouted it out loud. Often.

At the same time, the Morrison government has vocally supported the U.S. regardless of whether Trump or Biden have been at the helm.

And China has retaliated in the same fashion, but with more modern characteristics than it has used in the past.

The combination of a seemingly responsible clear skies policy and Xi’s belt and road directive provides a strong platform for China to squeeze many of its neighbours.

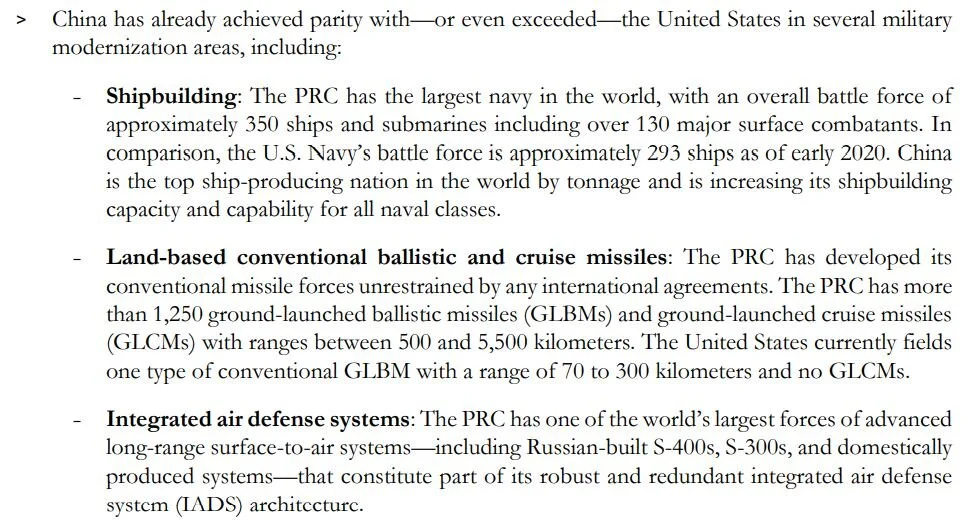

Here’s a snip from the U.S. Office of the Secretary of Defence, Annual Report to Congress: Military and Security Developments Involving the People’s Republic of China:

And the increasing investment in the Party’s war machine is one of the key reasons U.S.S Mercantile is getting a lot more anxious, and rallying its allies.

A quick look at China’s investment in fixed assets for the first half of the calendar year (January to June) in comparison to the same period in 2020, confirms some of that fear.

You won’t be surprised to know that the biggest increase in the rate of investment, up by ~30% plus, occured in railway, shipbuilding, aerospace and other transport equipment manufacturing. Spending in that category was 3.4 times higher than across all industries.

What now?

The trade war has reached a new level.

Markets are likely to become a lot more volatile over the coming weeks and months as both superpowers (i.e., U.S. and China) trade blunt instruments directly, and indirectly through others who become the proverbial meat in the sub.

You can already see it in ASX quoted stocks, and of course in commodities.

Iron ore spot prices have been falling for the past three months, which you would know about if you’ve been following my Game of Iron series.

In addition, China’s debt laden Evergrande appears to be having more problems with its debt stack and that’s sending some disturbing signals through markets.

Too big to fail? Or too big to save? We shall see.

And Australia’s relationship with the EU’s second largest economy may remain strained for quite some time. We shouldn’t be expecting any special deals on macaroons or Dijon mustard any time soon. Shame.

Your corporate strategy.

But back to home turf and to WA business owners that are looking to raise capital and/or engage in a merger or sale or special situation investment - here are some thoughts:

Equities are likely to become more volatile in their own right, not as a result of option trading and short squeezing, and there may be some nervousness amongst institutions and banks

Treasurer Frydenberg is likely to come down hard on inbound investment and M&A transactions where Chinese investors/bidders are involved

The Australian dollar may weaken given: Australia’s export customer concentration risk, China retaliation, and an increase in sovereign risk as a result of the way we have treated France. Although for there to be a material reduction in our currency pair the U.S. dollar would also have to strengthen, which it might if there is a flight to the reserve currency if emerging markets get hit

More special situation opportunities are bound to arise for corporate investors, and there’s plenty of cash around in private equity and treasuries to capitalise on these deals as and when they arise

It’s probably worth calibrating the above into your strategic, financing and corporate growth plans and keeping both antennae up for an opportunity to build your next edge or advantage!

Mike.

Next Level Corporate Advisory is a leading M&A and capital markets advisor with a 20 year track record of delivering the highest quality of independent financial advice as well as strategic transactions to help our clients level-up.

All text in this article is copyright NextLevelCorporate.