The divine comedy of inflation, done three ways

“Divine Comedy of Inflation.” (c) 2026. Prompt by NextLevelCorporate. All rights reserved. Image generated by AI.

TL; DR

On 14 May 2026, Federal Reserve Governor Michael Barr gave a speech defending the Fed's $6.5 trillion balance sheet.

It was technically competent. It was also, in important ways, incomplete. It was the kind of speech that is careful about what it says and more careful still about what it omits.

Barr used one word to describe the creation of bank reserves. The word was "costless."

In a narrow technical sense, he was right. Creating reserves costs the Fed nothing. No raw material, no printing press, no labour. The cost is simply moved: distributed invisibly, continuously, across every person who holds money, earns money, saves money, or prices goods in money. It does not appear on any balance sheet. It is not subject to a vote. It arrives not as a bill but as a slow erosion, the kind you only notice when you try to buy something you could afford last year.

That observation about one word in one speech opens into something larger and more important than the speech itself.

It opens into a question most people have never been invited to ask: what is inflation, really? Not the word as used today, in central bank press releases, in the speech of any central bank governor anywhere. The word as it was originally understood, before it was quietly reassigned to serve more convenient institutional purposes.

That reassignment is the subject of this article. Barr's speech is just the occasion for it.

The word they quietly stole from you

For most of monetary history, "inflation" meant one thing only: “The expansion of the money supply.”

That was it. Rising consumer prices were called "rising prices." And inflation described the act of inflating the currency, which is to say creating more claims on the same amount of real output, and it was understood to harm every holder of that currency immediately.

The historical parallel was exact: clipping coins, diluting gold with copper, minting five coins from metal that should have made four. The mechanism was debasement. The victim was whoever carried a coin.

Sometime in the 20th century, under institutional pressure from governments and central banks that needed a more manageable definition, the word shifted. "Inflation" came to mean rising consumer prices. Specifically, a government-published index, of a government-selected basket, measured by a government methodology that has been revised, repeatedly, in ways that consistently produce a lower number.

The swap seems technical. It is not. It determines who is accountable, when, and against what measure.

Under the original definition, a central bank that expands the money supply is immediately accountable. The debasement is complete at the moment of creation — visible, attributable, done. But under the new and more convenient definition, the same central bank is only accountable 12 to 24 months later, after the consequences have fully materialised, against an index it has significant influence over.

The definitional shift is not an accident of language. It is the most consequential piece of institutional self-protection in the history of modern finance.

And once you see it, you can’t unsee it.

The real point here is that "Inflation" was redefined from money supply expansion to consumer prices. That single swap moved accountability 18 months downstream — and shifted the cost from the government — onto you.

Now let’s see what it looks like from the inside.

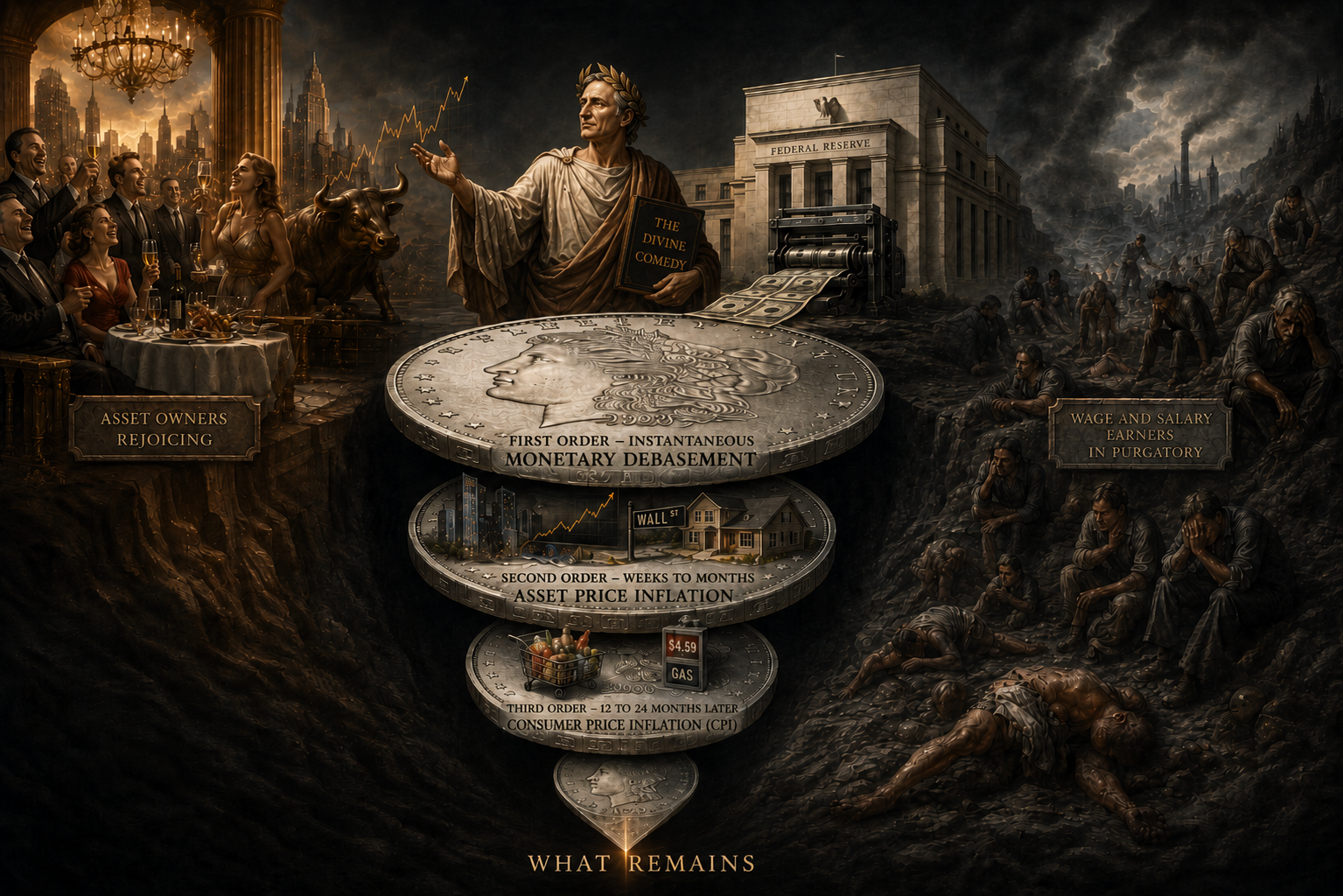

A guided tour — Dante’s divine comedy, and the three circles of inflation

“The Divine Comedy of Inflation.” (c) 2026. Prompt by NextLevelCorporate. All rights reserved. Image generated by AI.

In Dante's Divine Comedy, the writhing souls in his vision of Purgatorio do not suffer for their own sins alone. They work through consequences set in motion by others, climbing slowly toward something better while paying a price they did not individually choose. It is the right frame for what follows. Because the three circles of inflation are not entered voluntarily. You are born into them.

Our Virgil, as we descend, is the original meaning of the words “inflation,” which from our discussion above means: “The expansion of the money supply.”

Let those words be your guide as we descend.

The First Circle, Monetary debasement — instantaneous

This is where it begins, and where it ends before most people know it has started.

The moment a central bank creates new money, whether by printing reserves, purchasing bonds, or crediting bank accounts, the total stock of monetary claims expands. The money supply expands.

Every existing dollar of savings, every existing dollar of wages, now represents a fractionally smaller share of the same underlying output. The debasement is instantaneous and mathematical. It requires no lag, no transmission mechanism, no grocery price to rise. It is complete at the point of creation.

The historical analogy is exact. Four gold coins and one silver coin, melted together and minted as five, each still stamped as gold, each now worth 80 cents in the dollar of what it was. Today the process is digital, a keystroke at a central bank rather than a furnace in a mint, but the mechanism is identical. More claims, same output, each claim worth less.

Even though central banks never use the word this way. and Governor Barr does not mention it at all this is inflation in its original and native sense.

The Second Circle, Asset price inflation — weeks to months later

New money doesn’t arrive everywhere at once.

It flows through the financial system in a fixed sequence, banks first, capital markets second, the real economy last. This is what the 18th-century economist Richard Cantillon described in 1755, and what now bears his name, the Cantillon Effect.

In the weeks and months following monetary expansion, the first recipients of new money deploy it into assets, shares, property, bonds, credit instruments, before the broader price level has adjusted. Those assets reprice upward, absorbing the new liquidity while the purchasing power gain is still intact.

By the time the money reaches wage earners and retail consumers, prices have already moved. The early recipients, banks, asset holders, those closest to the source, have captured the real gain. Everyone else receives the money after its advantage has been spent.

This circle does not appear in CPI because asset prices were deliberately excluded from consumer price indices. And you will often hear the Fed Chair saying that the Fed does not look at or consider assets prices. Convenient, right?

The transfers that occurred during 2020 and 2021, as shares and property rose dramatically while the money supply expanded 41% in under two years, registered as precisely zero in the official inflation record.

The second circle is where wealth moves. Most people live their entire financial lives without knowing it exists. Afterall, according to prior Fed Chairs, the fault lies with “irrational exuberance,” not the Fed.

The Third Circle, Consumer price inflation — 12 to 24 months later

Here is the circle you’ve heard of. Here is what the evening business newsreader calls inflation. It’s what central banks are measured against and what Governor Barr's speech is ultimately about.

By the time consumer prices rise, the Virgillian descent from the first circle is complete. The debasement occurred instantaneously. The asset price transfer occurred over months with debasement jumping into asset prices. Now the excess money finally shows up in the price of groceries, rent, and energy. The redistribution and cost allocation is finished. What remains is the bill arriving at the table after the meal has been eaten and the diners who drank all the chianti and ordered the most, have quietly left.

But the Fed then raises interest rates to "fight" this inflation, taking credit for slowing a consequence of its own earlier actions, measured against an index that excluded the first two circles entirely. This is what "price stability" means in the language of central banking. Stability in the third circle, after the first two silent taxes have done their work.

And there is a further problem with the measure itself. CPI uses hedonic adjustments, which is to say that your new phone is "better," so the price rise is discounted. It uses substitution, if steak is too expensive, the model assumes you eat chicken, so the index tracks an adjusting standard rather than a fixed one. Geometric weighting, introduced in the 1990s, produces a structurally lower number than the arithmetic method it replaced. The Chapwood Index, tracking actual price changes of the 500 most commonly purchased items across 50 American cities, has consistently shown 8% to 12% annual inflation in periods when CPI reported 2 to 4. Every methodological revision has moved in one direction. The ruler was designed by the institution being measured. Another convenience that’s never explained.

Inflation done three ways, on one chart, minus circle 2

The chart below maps a Divine Comedy of Inflation onto a single frame of data.

Fig. 1 · NextLevelCorporate

Inflation, done three ways — M2 broad money, ON RRP balance, and CPI 2020–2025

First circle (M2 bars): monetary debasement — instantaneous. Blue bars show M2 expanding 41% from $15.4T (Feb 2020) to $21.7T (Apr 2022), resuming to a new record $22.4T by December 2025.

First circle overflow (ON RRP dashed): excess reserves parked back at the Fed overnight — $2.55T at peak, December 2022. When this drained through 2023–24 it re-entered the system as a second wave of first-circle liquidity.

Third circle (CPI amber): consumer prices, arriving 12–18 months after the M2 peak — exactly as the monetary transmission mechanism predicts.

Second circle: asset price inflation — absent from this chart because it was excluded from the official measure. That absence is itself the argument.

Sources: Federal Reserve H.6; FRBNY; BLS CPI. © NextLevelCorporate.

And here’s how to read it.

The blue bars are the first circle — M2, broad money — and each bar rising is monetary debasement occurring in real time. M2 grew 41% from $15.4 trillion in early 2020 to $21.7 trillion at its peak in April 2022, before resuming its climb to a new record of $22.4 trillion by December 2025.

The green dashed line is also the first circle, but its overflow. At its peak in December 2022, $2.55 trillion in reserves sat overnight in the Fed's reverse repo facility — money the Fed had created, which banks and money market funds handed straight back because there was nowhere productive to deploy it all. The Fed paid them interest to hold it. When that balance drained back into the system through 2023 and 2024, it re-entered as a second wave of first-circle liquidity, feeding asset prices before eventually reaching deposits and lending. Two rounds of first-circle debasement from one policy cycle. Good work ex-Fed Chair Powell.

The amber line is the third circle — CPI, arriving 12 to 18 months after the M2 peak, exactly on schedule. What is not on this chart is the second circle.

What is not on the chart is the second circle (asset price inflation) and that’s because it was excluded from the official measure. That absence is, in its own way, the most important thing on the page and one of the greatest cons of modern economics.

The point here is that by the time your grocery bill rises and shows up in main street CPI, the transfer (or misappropriation) of wealth through the first two circles is already complete.

And yet, the Fed is only accountable for the last echo of a process that began long before.

Two drivers, one train

One more thing before we surface, and it’s the thing that makes this a political problem, not merely a monetary one. The three circles are not created solely by the central bank. There are two distinct sources of monetary expansion, two rail lines feeding the same network, and both were running at full pressure simultaneously in 2020 and 2021.

The first is the monetary rail: the Fed creating reserves, purchasing bonds, enabling bank lending, filling the first circle from the top down.

The second is the fiscal rail: the government running a deficit, issuing bonds, spending the proceeds. When Treasury spends, fresh money lands in private bank accounts. Commercial banks lend against those deposits. The money multiplier runs. Broad money expands — not because the Fed did anything, but because the government spent more than it collected. This is debt monetisation: government liabilities converted into circulating money through the banking system, feeding all three circles from a separate track.

In 2020 and 2021, the US federal government ran deficits of $3.1 trillion and $2.8 trillion respectively — the largest peacetime deficits in American history — while the Fed ran quantitative easing at full capacity, buying the very bonds Treasury was issuing. Both rail lines were open for business. Both were creating money. Together they drove M2 from $15.4 trillion to $21.7 trillion in under two years. The third circle arrived on schedule.

Thus, the government cannot credibly blame the central bank for inflation its own spending initiated. And the central bank cannot claim to be a neutral technical actor when it is the primary enabler of fiscal excess.

Still, in Barr's speech, the word "deficit" does not appear once.

When a government runs trillion-dollar deficits and the central bank suppresses yields to make those deficits serviceable, the result is as inflationary as direct money printing — because it is, through a slightly longer route, precisely that.

— Two rails, one network, NextLevelCorporate

To summarise, the government runs the fiscal rails. The Fed runs the monetary rails. Both create money. Both filled the three circles. Only one appears in Barr's speech — and neither says the word "deficit."

And if you’ve been following my work on Treasury if Fed, Fed is Treasury, you will know that Treasury is now driving that liquidity train, with a subservient Fed under new Fed Chair Warsh. More on that in the end notes.

The real cost of Barr’s “costless” balance sheet

So, can we put a cost on all of this?

Well, yes — and as I’ve written on several occasions, the math is straightforward.

Since the GFC, the Fed's balance sheet has grown from $870 billion in August 2007 to $6.7 trillion today — a compound annual growth rate of 11.5% over 18.75 years. That is the institutional rate of first-circle debasement: the rate at which new monetary claims have been created, diluting every existing claim you hold. Add the average annual CPI of 2.5% over the same period — the third-circle cost arriving at your grocery bill — and the combined hurdle rate is 14% per annum. Every year. Since the GFC.

And you should note that when the balance sheet peaked a few years ago at $8.99 trillion, the figure was well above 14%.

But if you prefer the broader money supply measure, M2 grew from $7.5 trillion in early 2008 to $22.4 trillion by December 2025 — a CAGR of 6.6%. Add the same 2.5% CPI and the hurdle rate on that measure is 9.1%, giving a range of 9% to 14%.

But the Fed balance sheet method (14%) is the more honest number because it captures the full institutional rate of money creation from the true pre-GFC baseline. The M2 method (9%) is more conservative because it reflects only the money that actually multiplied through the banking system rather than sat as excess reserves. Both are real costs.

And the second circle that’s missing from CPI — second-circle asset price inflation — is the offset.

What this really means is that if your total return — capital growth plus income — has not been clearing somewhere above a pre-tax 14% each year since 2007, you have been moving backwards in real monetary terms, whether you knew it or not.

— The pre-tax required rate of return to beat inflation, NextLevelCorporate

Not because of bad luck or poor choices. Because the system extracted the difference, silently, through the two circles that never appear on the evening news. And that is precisely the real cost of Barr’s “costless” balance sheet.

Welcome to inflation purgatory

Dante's souls in purgatory are not there because they are wicked. They are working through consequences, slowly, without fully understanding the mechanics of why, and they are paying in time and suffering for a condition they did not solely create.

That is a reasonable description of what savers, renters, and wage earners have been doing for the past several years. They did not choose to have the word "inflation" redefined. They did not choose to have the costs of monetary expansion placed outside the measured index. They did not choose to be in the third circle while the transfers of the first two were completing around them. And many of them were denied the advantages of asset price inflation because they did not own any.

They arrived, as most people arrive in purgatory, already inside it.

Governor Barr's speech did not intend to illuminate any of this. But the word "costless" opens a door that, frankly, needs to be called out and explained for the massive con it is.

And now that the door is open, the tour is the thing. Now at least you can see it for what it is, what it costs, and the size of the annual bill you are footing.

See you in the market 🖐

Mike

Further reading from NextLevelCorporate’s, NextPerspective: TIFFIT — QE Infinity Train is Signal. New Fed Chair Is Noise — how deficits, debt monetisation, reserves monetisation, fractional banking, and monetary debasement combine into the only train that matters, and who is now driving it.

With decades of success across six continents, NextLevelCorporate helps you navigate the intersection of M&A, financial advisory, and business strategy —delivering macro-aligned corporate development strategies and the transactions that bring them to life.

All content is copyright NextLevelCorporate. NextLevelCorporate and logo are registered trademarks.