Metals Roundup Jun'26: honey we shrunk the copper bull

“Honey, we shrunk the copper bull” Copyright 2026. nextlevelcorporate. nextlevelcorporate prompts, AI generated image.

Summary for June 2026. Base metals give back some of the run

Well, we got the Trump TACO we were waiting for in the last edition of Metals Roundup, but we're still facing the reality of sticky inflation (which should start to hit agriculture and food prices), and Kevin Warsh isn't signalling rate cuts.

If anything, the June dot plot showed close to half the FOMC leaning toward a hike before year end.

Then last week's jobs number landed at just 57,000, the weakest U.S. print in four months, with a combined 74,000 knocked off the April and May figures on revision.

That spooked an equities market already stretched from the AI capex boom and the SpaceX IPO (the biggest listing in history 🤣 and a reminder of just how much froth is sloshing around right now). Bond markets moved fast.

The odds of a hike at the 29 July FOMC meeting had been sitting around 30% ahead of the report and dropped into the high teens within a day.

In turn, it's only been the last few days that the USD has started to weaken after months of strength. Could it strengthen again? Yes, if Warsh signals that inflation still needs fighting. On the other hand, a soft jobs print builds the case for a pause, and maybe even an adjustment cut later this year.

We won't know for a while, because as you know, No Dot Warsh isn't in the business of giving guidance.

Since I wrote that piece, No Dot Warsh has softened at the margin, telling the ECB's Sintra forum on 1 July that inflation risks "have come down," without committing to a direction either way.

More on what that's done to rates pricing and gold in Local Impact below.

But USD strength through April and May is the more likely culprit for what happened to base metals in June, not a sudden June shock, but the third straight month of cooling.

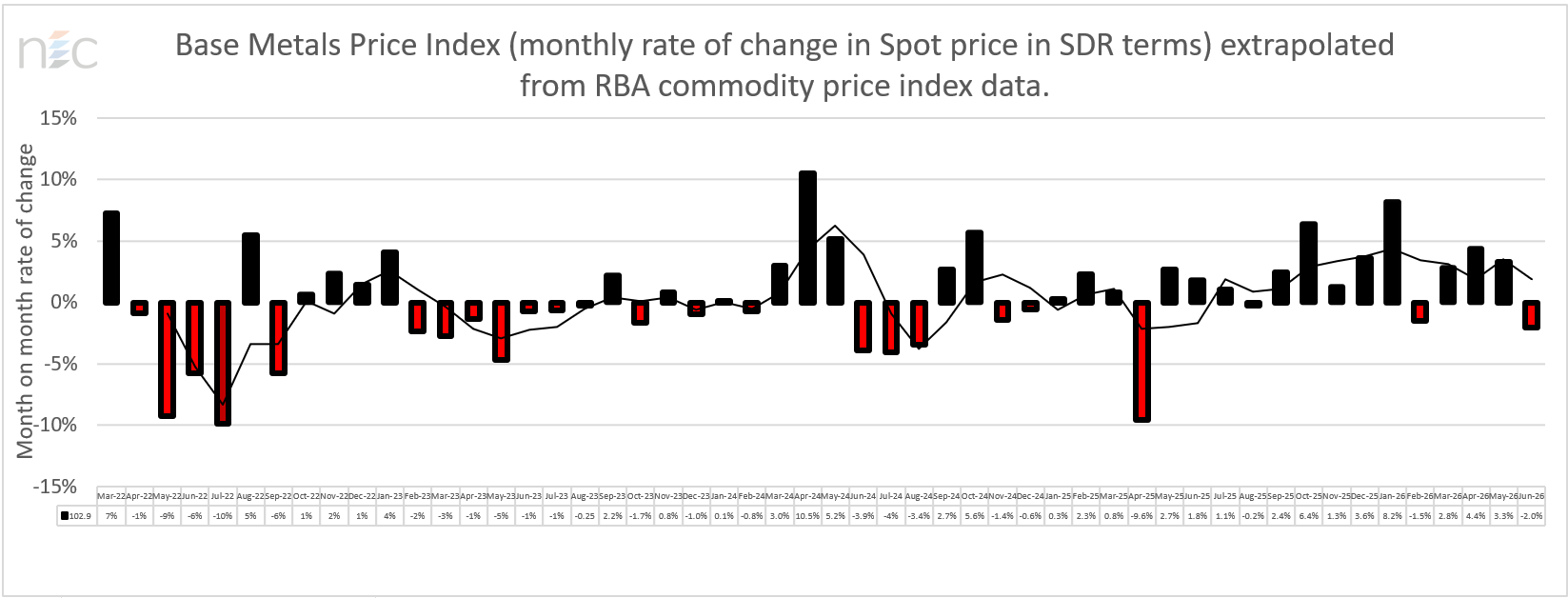

The RBA's base metals index (copper, aluminium, zinc, lead and nickel in SDR terms) peaked at +4.4% in April, slowed to +3.3% in May, then flipped to, 2.0% in June, a swing of 5.3 percentage points in a single month, and the first negative print since April 2025. Copper is the heaviest weight in that basket and the most likely swing factor, but it's worth being precise, because this is a base metals story, not a copper-only one, despite the shrinking copper bull above.

The massive sovereign debt refinancing Treasury Secretary Bessent has in front of him, something in the order of $8-10 trillion in rollovers this year, is the backdrop for the "Plaza II" idea I keep coming back to. Which is to say some kind of multi-sovereign accord to engineer a weaker USD and make that refinancing more affordable, in and out of the US. Some economic commentators have been talking about Plaza 2.0 or Plaza Accord 2 for some time now, however, and to be intellectually honest about this, this is my read of the incentives, not something anyone in Washington has confirmed. That said, it is also entirely consistent with my TIFFIT framework, especially while the concept of QE remains “on the nose,” as it does for Warsh.

The byproduct of Plaza II, if it happens, would be cheaper USD-denominated commodities for China and Europe, and a more synchronous global growth picture. AI infrastructure buildouts included. Almost every sovereign is incentivised to see a lower USD.

If I'm right, the commodities super cycle resumes if and once Plaza II gets locked in.

Today, let's dig into the monthly rate of change charts to see what actually happened with industrial metals and minerals in June 2026, and why I don't think the USD is the whole story.

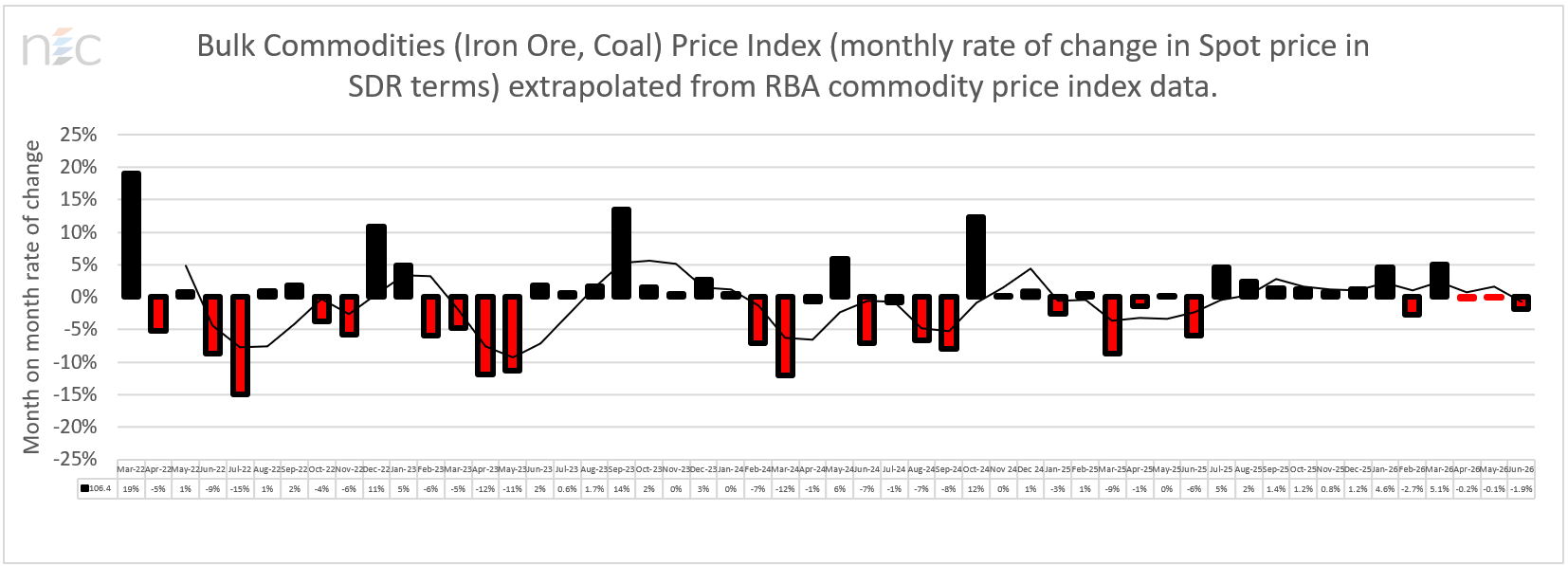

Base metals vs. bulks, the divergence is the tell

Here's the thing that jumps out when you put the two charts side by side.

Copyright, NextLevelCorporate Advisory

Copyright, NextLevelCorporate Advisory

If a weakening-then-strengthening USD were the dominant driver of both baskets, you'd expect base metals and bulk commodities (iron ore, coal) to move together. Same currency channel, same rough timing.

They haven't.

Bulk commodities have been flat-to-negative for three straight months: April –0.2%, May –0.1%, June –1.9%. Meanwhile base metals were still posting solid gains through April and May before June's reversal. If USD strength alone explained June's base metals pullback, bulks should have caught a similar tailwind on the way up in April-May, they didn't get one.

That divergence points to commodity-specific demand stories layered on top of the currency effect:

Bulks are the China-construction proxy, and construction is still soft. Iron ore and coal are much more directly tied to Chinese steel output and property activity than base metals are. Beijing's "anti-involution" push to rationalise steel capacity, plus a property sector that still isn't showing a durable recovery, is a more parsimonious explanation for three flat-to-down months than anything happening to the dollar.

Base metals had their own supply-side story driving the January-April run, separate from currency, mine disruptions and tight refined-copper availability pushed base metals up 8.2% in January alone. Some of June's giveback looks like ordinary mean-reversion and profit-taking after a four-month run, on top of the USD move.

Positioning matters more than people give it credit for. After a run like Jan-Apr, CTA and momentum flows can amplify a turn once it starts, i.e., the reversal doesn't need a fresh fundamental shock, just enough of a wobble to trigger unwinds.

Freight and seasonal effects on bulks specifically. Pilbara iron ore shipments are exposed to wet-season and cyclone disruption on the supply side, which can move the index independently of demand.

China, Korea and Japan are the destination markets for both baskets, but tariff-related trade-flow uncertainty (still working through the system post-TACO) probably weighs more heavily on the bulk/steel supply chain, as does China's centralised buying of iron ore, than on base metals, which have alternative buyers (EV, grid, data centre build-out) less exposed to the tariff conversation.

But to be clear, none of it rules out the USD/Plaza II thesis. In our thesis, a weaker USD is a real and probably necessary condition for a broader commodities' re-acceleration.

But June's base metals reversal looks more like the unwind of an overextended four-month run, due to data centre-driven capex spending pulled forward, than a single-month currency shock. That plus the bulks weakness has been building for longer than the USD narrative alone accounts for.

Other industrial commodities of interest

⚗🧲☢ Energy minerals (ex-coal and oil)

The July 6, 2023, price high for LME Lithium Hydroxide CIF was US$46,046.

On the last LME trading day of June, it printed US$19,500/t, a monthly price collapse of 10% and still more than 58% down from its July 2023 peak. Petroleum supply shocks and shortages leading to some substitution/switching to EVs had been driving the increase but since the Trump TACO on Iran the pain seems to be a memory. I don’t believe we have seen the last of troubles in Hormuz and the region.

On the other hand, sodium and other battery chemistries are being spoken about more often, with higher levels of confidence for certain applications.

But like rare earth prices, floors and geopolitical-driven support, lithium prices are likely to fall further under a geopolitical “kiss and make up” scenario.

Uranium was trading 50c/lb lower at the end of June than in May, indicating solid support at the June level of US$85.5/lb. I expect uranium prices to continue “up to the right” although not in a straight line. And I continue to note uranium is not controlled by China and is a purer form of exposure to zero-emissions electricity, plus the energy hungry AI chip and data centre build out.

Fossil fuels are now more than ever making a structural comeback as I’ve been suggesting. And as predicted last month, Russian oil is now freely traded and the U.S. is likely going to let China have more oil, for a strategic price, if we see a Plaza II accord.

🪔 Oil

On February 28, 2026, the United States and Israel launched coordinated airstrikes on Iran under Operation Epic Fury, targeting military facilities, nuclear sites, and leadership. The response was swift and economically devastating. Shipping traffic through the Strait of Hormuz virtually ground to a halt with a handful of vessel movements.

That narrow passage through which around a fifth of global oil production flows, and which also, as few people appreciate, transits around 45% of global sulphur exports needed in the production of fertiliser. Add to that Iran's missile attack on Qatar's Ras Laffan (the world's largest LNG liquefaction plant) causing extensive damage to Qatar Energy's infrastructure, and halting ~330m m3 of LNG/day (20% of global trade) via the Strait. You can read more here.

Those ructions are slowly dissipating, and we are yet to see price shocks from the oil and fertiliser supply shock flow into agriculture and food prices. But we will.

At the end of June, Brent crude and West Texas Intermediate were trading at ~US$72.95 and ~US$69.50 per barrel, respectively, with Brent down a substantial $20 per barrel down from last month.

No matter the oil price, energy companies will still make money, just at different point of their value chain.

One live wrinkle as I write is that Iran's former Supreme Leader Khamenei has died, and today's funeral has paused the next round of Doha talks right as Hormuz flows had pushed back past pre-war levels. De-escalation was starting to look entrenched. It isn't yet, and a leadership transition in Tehran is not the moment to assume the Hormuz story is closed.

Local impact from global forces

At a macro level, global liquidity is still recalibrating, but the shape of the recalibration has changed since last month.

The USD just had its worst week since April, gold has found a bid back above US$4,150/oz after cooling off January's US$5,597 peak, and rate-hike odds for both the 29 July and September FOMC meetings have fallen sharply on the back of that soft jobs print.

No Dot Warsh himself, speaking at the ECB's Sintra forum said inflation risks "have come down" as energy prices eased following the Iran ceasefire. This was a materially softer line than the one he was running in June, even though he still won't commit to a direction. The market read it as the door to a cut is open a crack wider than it was a month ago, but nobody's walking through it just yet.

The wrinkle nobody had priced a week ago is Tehran. Iran's former Supreme Leader Khamenei has died, and today's funeral has paused the next round of Doha talks right as Hormuz flows had pushed past pre-war levels and Brent/WTI had round-tripped back down to the low-$70s and high-$60s. De-escalation was starting to look entrenched. It isn't yet. I'd treat the current oil complex as priced for a peace that's real but not finished, which is a fragile place for it to sit heading into a leadership transition in Tehran.

Aside from AI infrastructure, chips, the critical minerals required to power them, and now space (and soon, likely, foundation models themselves), most other equities and crypto are still range-bound. Add to that the ongoing difficulty in sovereign debt refinancing markets while the dollar, even after this week's wobble, remains firm on a 12-month view.

Strategy

This is what the current macro spells out for your corporate development and investment strategies, if you're in Australia.

Corporate development strategy. I continue to see the macro affecting certain mineral projects as a result of discounting future cash flows at higher rates, inflated capex, and borderline debt serviceability. In its place, more M&A. This is accelerating. Capital is selective, but for favoured sectors, gold, rare earths and uranium, it's strong, even with lithium down another 10% on the month. This can change quickly, especially for metals that behave cyclically even though the long-term thesis is still intact. If the Fed does lean dovish off this jobs print, that's a genuine (if still speculative) tailwind for feasibility studies on the margin, don't build a deal around it yet, but it's worth modelling. Watch unemployment from ageing demographics and AI substitution, and watch where the AI IPO wave pulls capital from, more on that below.

Investment strategy. This week's soft jobs print and Warsh's easier tone at Sintra have added to the dollar's worst week since April. For the moment, under this Administration, the wind is coming out of the petrodollar's sails. Some green shoots in global liquidity are visible, gold's bid off its June lows is one sign, but Khamenei's death and the paused Doha talks are a reminder that the Hormuz story isn't closed, and a re-escalation there would move oil, fertiliser and sentiment fast. Are we in a bubble? The market didn't fall out of bed over the SpaceX IPO, but it wasn't clean either, SPCX has given back roughly a third of its post-listing pop, from over US$225 back to around US$153. That's the live template for what Anthropic (tracking an October listing at a ~$965bn valuation) and OpenAI (now leaning toward 2027) will face if and when they list, and it's worth watching as a rotation risk for the Magnificent Seven rather than a crash risk, money moving into new listings has to come from somewhere. . Like last month, equities capitulation and peak yields are still not in, we're not done yet, so we wait. Crypto capitulation has probably already happened. Liquidity is steady but not stimulative, so a bubble and crash is unlikely.

Overall, the full effects of 30 January 2026 (the Kevin Warsh nomination and accelerating inflation), the softer tone he struck at Sintra, and the still-unresolved situation in Iran, are all still whipsawing their way through financial and commodity markets, in different directions, all at once. It’s not easy to predict.

In the meantime? Hard commodities super cycle on pause, interest rate cuts/hikes on pause but tilting slightly more dovish than a month ago, and plenty of project and investment volatility until further notice.

See you in the market 🖐

Mike

Macro first. Strategy second. Deal third.

An independent corporate development studio, established in Perth in 2001, advising you when — and when not — to do the deal. In 25 years, that discipline has been the difference.

This content is copyright NextLevelCorporate. It is not advice and it is provided for informational purposes only. NextLevelCorporate and logo are registered trademarks. All rights reserved.