TIFFIT Confirmed! Kevin Warsh Read My article

Image generated by AI, prompt by NextLevelCorporate.

TL; DR

Kevin Warsh's confirmation hearing last week was supposed to be about who the next Federal Reserve (Fed) Chair is. Instead, it turned into an accidental proof-of-concept for my working thesis that I first wrote about and coined in May 2024: TIFFIT — Treasury Is Fed, Fed Is Treasury.

Under TIFFIT, the Treasury controls systemic liquidity. And while the Fed still has tools like quantitative tightening (QT), quantitative easing (QE) and reserves management, Treasury uses its own tools in response to Fed policy to influence systemic liquidity. It also coordinates with other departments to relax prudential regulations such that the private sector now takes over from the Fed in supporting Treasury issuance. Through this coordination, Treasury becomes the new driver of the QE Infinity train to nowhere — which is my metaphor for what most people call ‘money printing.’

Think of it as a train that never stops, carrying a highly coordinated cargo of fiscal and monetary liquidity for markets, but where the Treasury Secretary (responsible for refinancing close to $40 trillion of government debt) and not the Fed Chair, gets to drive it.

Warsh, who is Trump's nominee and while not yet confirmed is clearly backed by the White House and Treasury, confirmed: (a) Fed-Treasury coordination on balance sheet normalisation, (b) preference for rates over QE (quantitative easing), and (c) a supporting role for the Fed behind the dollar and Treasury, and relaxed banking regulations.

I think he’s been reading my articles. Still, whether he gets the job or not, what he said under oath before the Senate Banking Committee this week was more revealing than any Fed minutes in recent memory. Warsh never mentioned stealth liquidity, nor TIFFIT. But then again, he didn't need to. His testimony confirmed that it’s very real.

For investors, the implications are concrete: deregulation of aspects of Dodd Frank, balance sheet shrinks, rates come down, net liquidity rises, private banks become active buyers of Treasuries, bonds rally, AI and crypto get a second wind, and US productivity gets a turbocharger.

But inflation and uncertainty haven’t left the building as we discussed in the last edition (linked below).

If you want to know what it all means, read on.

Well, that was unexpected but validating

I want to be clear that I did not brief Kevin Warsh before his Senate confirmation hearing this week.

I also want to be clear that if someone had handed him a copy of my last article on TIFFIT and asked him to read selected passages into the congressional record, the result would have looked roughly similar to what actually happened.

Warsh didn't use the word TIFFIT. But he didn't need to. What he described is TIFFIT in a suit and tie, sitting under oath before the Senate Banking Committee. And that is a Fed that works with the Treasury on balance sheet normalisation, steps back from QE as a routine tool, and positions itself as a supporting player to the dollar and Treasury's objectives. Treasury is Fed, Fed is Treasury. Q.E.D.

Before we go further, it’s fair to point out that as of the time of writing, Warsh has not yet been confirmed. His path through the Senate was until last Friday complicated by a Republican senator withholding his vote over a separate DOJ investigation into current Fed Chair Powell. It’s a subplot that says as much about the politicisation of the Fed under Trump as anything Warsh said during the hearing itself. The probe into Powell as dropped on Friday. Warsh is now widely expected to be confirmed. But here's the point. It doesn't actually matter whether he gets the job. What he said at that hearing confirmed the structural framework regardless of what his business card eventually says. TIFFIT doesn't need Warsh to be confirmed. It just needed him to speak to prove it exists and is being worked towards.

So, no, I'm not saying I told you so. I'm simply noting that my TIFFIT framework and investing lens appears to be holding up rather well. Don’t believe me? Watch the confirmation hearing on YouTube and then look at the price action response in bond and equities markets since then. One word? Yippee-ki-yay…

TIFFIT's coming-out party

Let's be precise about what Warsh actually said at his 21 April hearing, because the signal here is unusually clear.

He confirmed he would be working slowly, deliberately, and in close coordination with Treasury Secretary Bessent to reduce the Fed's balance sheet. His words were choreographed, well-orchestrated, and designed to limit unnecessary market disruption.

That is not the language of an independent central bank acting unilaterally. That is the language of a co-pilot who knows exactly who’s flying the plane, or better still, the second man in the fireman’s seat next to the engineer (aka the Treasury Secretary) driving the TIFFIT-QE Infinity Train to nowhere.

Warsh also said the Fed should play a supporting role to the Treasury in reinforcing confidence in the US dollar. Not a parallel role. Not an independent role. A supporting role.

For those who have been following my TIFFIT thesis since I first coined it in May 2024, this is not a subtle development. As a small refresher, here is what I wrote earlier this year in “In 2026, TIFFIT-QE Infinity Train is Signal. New Fed Chair Is Noise”.

"TIFFIT results in a sidelined Fed and a powerful Treasury Secretary. By managing the level of Treasury deposits within the banking system and adjusting for whether the Fed is adding or withdrawing reserves through QE or QT, Treasury can exert significant influence over broad money growth (M2), system net liquidity, credit creation, and capital allocation. And since refinancing sovereign debt is priority number one, Treasury will pull levers to create more net liquidity and/or a lower cost of capital. With this will come more debasement of currency, loss of purchasing power, and asset price inflation."

Warsh didn't quote that back to the Senate Banking Committee. He just described it, in his own words, under oath. The result is that the institutional architecture I’ve been describing since 2024, in which the Treasury drives systemic liquidity, the private sector banks take over from the Fed in anchoring the repo market while the Fed manages around the edges, has just been endorsed in principle by the incoming Fed Chair nominee himself.

If confirmed, the TIFFIT-QE Infinity Train to nowhere will have a new engineer driving it, and Warsh, his soon to be second man in the fireman’s seat just confirmed both the route and the timetable to nowhere, even if he's never heard the name of the train. And why “nowhere”? Because the train CANNOT stop, lest it destroy the global collateral base underpinning the Eurodollar market that supports ~$350 trillion in global debt, with just under 1/3rd of that stack being sovereign debt.

The Balance Sheet retreat and why it hands power to Treasury and commercial banks

Warsh's case against QE as a standing tool of monetary policy is worth dwelling on, because it’s both intellectually honest and structurally significant. And under my TIFFIT framework, any change to the balance sheet can be compensated for in terms of net liquidity by a Treasury tool in order to achieve the Treasury’s desired outcome,

His argument runs as follows. QE works through two channels, a signalling effect, and financial asset price inflation. The second channel is the problem. When the Fed expands its balance sheet, it pushes up the prices of financial assets. That's fine if you own financial assets. Roughly half of Americans don't. QE therefore distributes its benefits upward, which is a distributional consequence that is not, and should not be, the domain of the Federal Reserve.

He went further when he described QE as fiscal policy in disguise. He noted that holding long-term Treasury assets blurs the line between monetary and fiscal authority and pulls the Fed into politics, which is a place it has no business being. He acknowledged his own role in the 2009 QE response to the GFC but emphasised that it was authorised as an emergency measure, predicated on rates being pinned to zero. The emergency passed. The balance sheet didn't. And Bernanke, as Warsh might have said more diplomatically than I will here, never quite got around to paying it back.

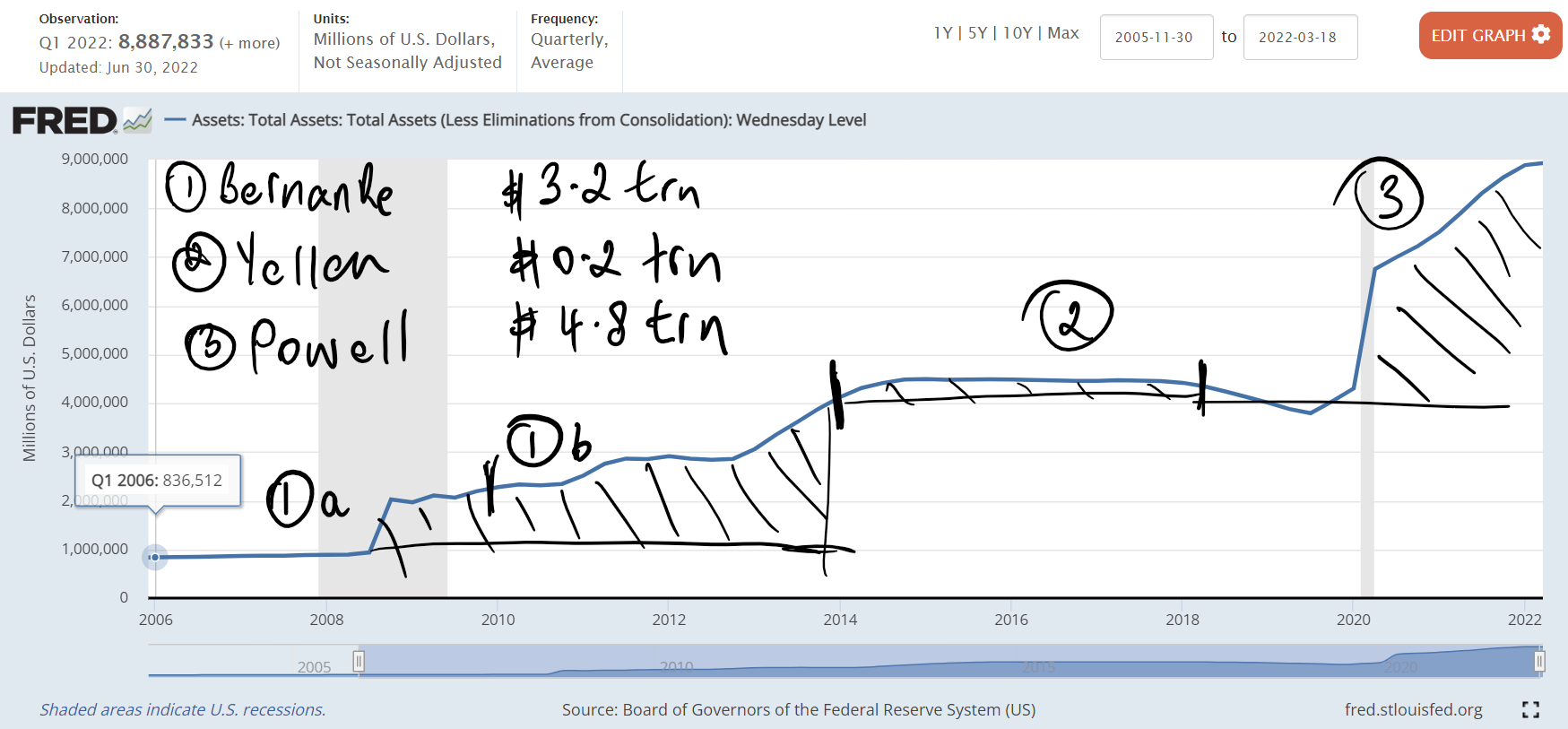

And in support of that, below you will find something of a flashback I put together in June 2022. It shows the Fed’s balance close to its peak level of $8.9 trillion. But more importantly, it shows the starting level of $836 billion in Q1 2006 (which Warsh cited at the hearing last week) and that Fed Chair Bernanke did the exact opposite of paying back the trillion. Instead, he added $3.2 trillion, growing the balance sheet by nearly 5x—well after the exigent circumstances had passed.

While pop your collar Chair Yellen only added $200 billion to the balance sheet (and by the way was also of the opinion that QE disadvantaged those who could not access its benefits), Chair Powell supersized it with his death star-like burst in response to COVID-19. Powell and Bernanke, notwithstanding their seemingly calm and collected demeanours, were addicted to the money printer.

Thereafter, the balance sheet peaked at $8.9 trillion, more than 10x the size it was back in 2006. That’s the factual history.

Fred data. NextLevelCorporate analysis.

Now, back to Warsh. Warsh’s preferred monetary tool is interest rates, which he argues get into the cracks and affects a broader cross-section of the economy. It does this by distributing the benefits of easier monetary conditions more widely than asset price inflation ever could.

Here is the structural irony that Warsh may or may not have fully reckoned with. By retreating from the balance sheet and handing that lever back, the Fed is not reclaiming independence. It is confirming TIFFIT. Because if the Fed steps away from QE/RMP and balance sheet management, the liquidity gap doesn't disappear. It migrates to Treasury, which fills it through TGA/reverse repo managed stealth liquidity, regulatory easing where commercial banks play a much bigger role (as they should), and the other mechanisms I’ve written about extensively in the context of the TIFFIT-QE Infinity Train to nowhere.

And one of those very important strategies will be the upcoming relaxation of regulations applicable to the eight largest U.S. banks which will allow banks to purchase Treasuries directly from the Treasury, bypassing the Fed. To the extent this deregulation passes, it will reshape reserve flows, increase systemic liquidity and effectively swap the Fed for the private sector as the anchor for the repo market (the single most important market for banks to manage their short-term liquidity).

As I wrote in the December 2025 article linked above, the proposed changes to the Enhanced Supplementary Leverage Ratio (eSLR) could release ~$2.1 trillion in balance-sheet capacity for Treasuries market-making, by the banks.

So, under a Warsh Fed, if confirmed, we will have a subservient Fed that will attempt to shrink its balance sheet in coordination with Treasury and the banks, which following regulatory easing via the eSLR, will have a greater role in supporting Treasury issuance, thus anchoring the overnight repo market and keeping the financial system well-oiled in a less inflationary manner.

And what this means is that the train doesn't stop, because it can’t. The driver just changes seats with the fireman. If Warsh is confirmed, Scott Bessent becomes the most powerful non-war time Treasurer, and the banks replace the Fed as the anchors of the overnight repo market.

Rates come down, but the rich will still win, both ways

With Warsh preferring rates as the dominant monetary tool, and with the direction of travel pointing toward normalisation, the implications for capital allocation of a Warsh confirmation are significant.

Lower rates mean higher bond prices. Duration becomes your friend. Investors who rotate out of equities into fixed income, and let's be honest, this rotation is already underway among those managing large pools of capital, will benefit as yields fall and bond valuations recover.

But here’s the part that doesn't get enough attention. Lower rates don't just benefit bonds. They also reprice long-duration equities, the kind whose value is most sensitive to the discount rate applied to future earnings. Think AI infrastructure, NASDAQ-heavy portfolios, and tech and other names that were most compressed during the rate-hiking cycle. Lower rates also provide fresh oxygen for crypto, which has increasingly correlated with risk-on liquidity conditions and long-duration asset repricing.

So the investor class, and Warsh was candid about this dynamic, will likely benefit on both ends of the rotation. Fixed income goes up as rates fall. Long-duration equities and digital assets also benefit from the same falling rate environment. The distributional consequences he described so clearly will not disappear simply because QE is being wound back. They will just arrive through a different door.

AI + lower rates = the U.S. productivity thesis

There is a second-order consequence of lower rates that deserves more attention than it is currently receiving in markets: the interaction between cheaper capital and AI-driven productivity.

Warsh himself noted that the U.S. is the best-positioned country in the world to take advantage of artificial intelligence. That's not a throwaway line. It's a policy signal.

Lower borrowing costs reduce the hurdle rate for AI infrastructure investment, i.e., data centres, energy, compute, and the enterprise software layer being built on top. When capital is cheap and the technology is ready to scale, you get adoption cycles that can move faster than most models predict.

The productivity implications are real. If AI delivers even a fraction of the efficiency gains being modelled across healthcare, logistics, financial services, and manufacturing, the U.S. could enter a period of genuine productivity-led growth. And that’s the kind that actually helps with the debt-to-GDP problem that the TIFFIT-QE Infinity Train to nowhere was designed to manage.

It also strengthens the dollar thesis. Warsh was explicit when he said policy should reinforce confidence in the USD by delivering stable prices, improving real take-home pay, reducing inflation, and positioning the U.S. as the world's highest-potential growth economy. AI is part of that story. A stronger dollar makes the global debt stack denominated in USD more expensive to service for foreign borrowers, but it also reinforces demand for dollar-denominated assets, which matters a whole lot for Bessent’s Treasury refinancing.

The productivity play and the dollar play are the same play, and lower rates are the accelerant.

But, as I’ve been saying, inflation hasn't left the building

There is a tension in all of this that Warsh identified with unusual clarity, and which investors would do well to keep front of mind.

When asked to define inflation, Warsh did not reach for a Phillips curve or a wage-price spiral. He said, essentially: inflation happens when central banks print too much and governments spend too much.

Read that carefully. That is a monetarist definition. And it is also, whether he intended it this way or not, a precise description of what the TIFFIT-QE Infinity Train to nowhere has been doing for the better part of two decades.

The balance sheet retreat will be slow and deliberate. Fiscal deficits are not going anywhere. Treasury issuance will continue at scale. The structural liquidity that has been injected into the system does not evaporate because the Fed stops adding to it. It circulates, it compounds, and it continues to put a floor under asset prices and a cap on purchasing power.

Consumer price inflation may prove to be sticky. And if the re-emergence of the term premium proves to be a structural feature of long-end yields, not merely a cyclical one as I proposed in last week’s edition: “Is the Bond Market Pricing Inflation or Risk?” then Warsh will face exactly the tension he described. And that is a preference for rates as the dominant tool, but a bond market that demands compensation for inflation risk and uncertainty at the long end of the curve.

That keeps a floor under the 10-year Treasury yield (and longer durations) which complicates the bond rotation story, and it means the Fed's ability to cut rates aggressively is more constrained than the lower-rates narrative currently assumes.

The TIFFIT-QE Infinity Train to nowhere steams on. But the track ahead has a few bends and some experimenting by Treasury, with the mix of issuance being a balancing act in terms of duration. And as for inflation, a smaller Fed balance sheet with the banks doing the heavy lifting (assuming regulatory changes are made) is likely to be less inflationary than using the Feds balance sheet. We shall see.

What Warsh told us without saying it

If you step back from the individual policy positions, the picture that emerges from Warsh's confirmation hearing is coherent and significant.

If confirmed, his Fed will step back from balance sheet expansion as a routine tool. It will coordinate with Treasury on the pace and choreography of normalisation. It sees its role as supportive of, not independent from, Treasury's objectives around the dollar, debt management, and economic positioning. It will embrace digital assets as part of the financial fabric (because “they already are”). And it will commit to humility in the form of fewer forward guidance signals, more reactive decision-making, and less FOMC theatre.

Every one of those positions is consistent with TIFFIT. Some of them are TIFFIT stated plainly in different language.

The framework I have been building since 2024, in which Treasury drives systemic liquidity, the Fed manages at the margins with commercial banks taking over from the Fed in the repo market, and the TIFFIT-QE Infinity Train to nowhere continues under coordinated management, was validated this week. Not by market data, but by the man Trump wants running (or caretaking) the Fed.

Confirmed or not, Warsh spoke. And what he said matters more than whatever the Senate eventually decides to do with his nomination.

What a Warsh confirmation means for you and me

If Warsh, or another similarly thinking Trump nominee is confirmed, my 2026 playbook for investors and corporate strategists remains intact.

That is to say that I see the TIFFIT-QE Infinity train to nowhere running on both monetary and fiscal tools engineered by the Treasury (in coordination with a weaker subservient central bank and more active private banks in the repo market) and designed to refinance sovereign debt and recalibrate net liquidity to a Treasury-desired state, while papering over a bankrupt planet.

This comes at a cost, namely more monetary debasement and loss of purchasing power for wage earners (P&L reliance), and stronger asset prices and returns for those holding real assets (Asset reliance).

In support of that:

Watch net liquidity flows and Treasury issuance/interventions, not Fed statements.

Watch for Dodd Frank and eSLR changes and banks buying Treasuries direct from the Treasury.

Position for lower short-end rates, AI-driven productivity, stronger dollar, and the continued inflation of real and financial assets, especially long-duration geopolitically aligned equities (tech, AI, supply chain, chips, energy, defence, etc).

Watch term premia build in long-duration Treasuries.

In Australian fixed income terms, if we see investment grade fixed income opportunities at or around the 7% level, there will likely be a rotation from Australian equities to fixed income, but for certain geopolitically charged material plays.

Hold real anti-debasement assets (precious metals, bitcoin, etc) and select commodities as a hedge against debasement.

And remember that in a system this coordinated, the noise is often loudest precisely when the signal is clearest and obvious. Don’t overcomplicate it.

Warsh never mentioned TIFFIT. But then again, he didn't need to. The TIFFIT-QE Infinity Train to nowhere knows its own name and where it’s going!

Good luck and see you in the market 🖐

Mike

With decades of success across six continents, NextLevelCorporate helps you navigate the intersection of M&A, financial advisory, and business strategy —delivering macro-aligned corporate development strategies and the transactions that bring them to life.

All content is copyright NextLevelCorporate. NextLevelCorporate and logo are registered trademarks.