Is the Bond Market Pricing Inflation or Risk?

…and what it means for Australian corporate development, M&A, and investment strategies…

TL; DR

After more than a decade of suppressed risk premia, something structural has shifted at the long end of the U.S. Treasuries yield curve.

At first glance, the rise in long-term bond yields looks like a familiar story, and with the 10-year Treasury trading on a yield of ~4.3%, the immediate instinct is to point to inflation. After all, higher inflation drives higher yields, right?

But the data is telling a more nuanced story, pointing to something more structural being built into the long bond yield. And if it is more structural, there are several implications for your corporate development, M&A, and investment strategies.

Let’s dig in.

Decomposing the long-term bond yield

Every long-term bond yield is made up of three things stacked on top of each other, like a burger:

Yield = Real rate + Inflation expectations + Term premium

Using that formula, let’s solve for today’s real rate (17/4/26), where Real Rate = Yield - Inflation Expectations - Term Premium, and we’ll use the 10-year duration because in finance, it’s what we use for the risk-free rate:

The US 10-year Treasuries Yield (the risk-free rate) is ~4.3%.

Using market breakeven rates, inflation expectations account for roughly 2.4% of that (well down on 3% in April 2022).

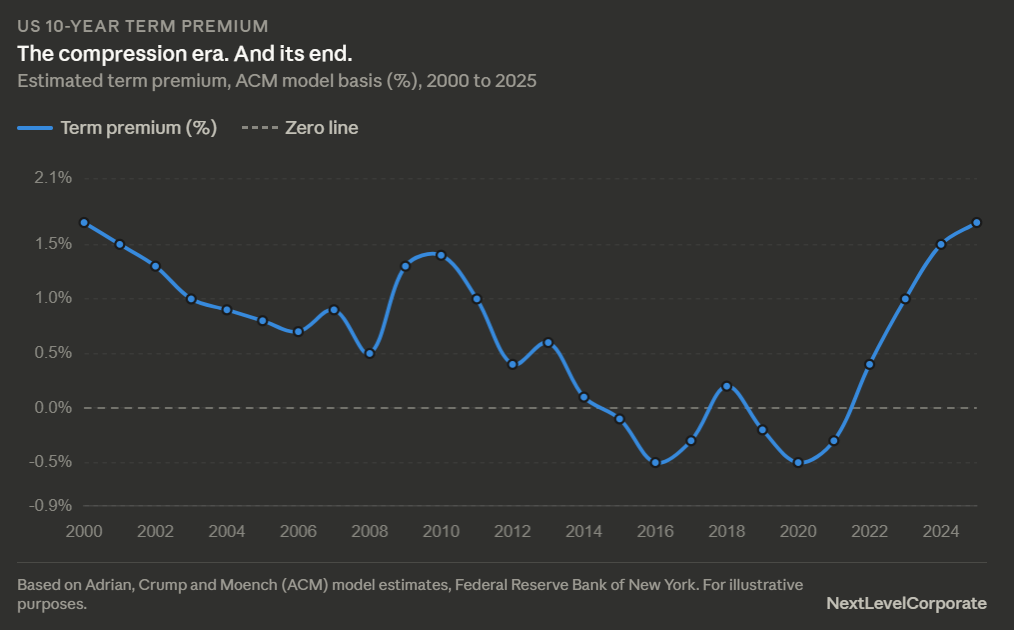

Using the New York Fed's ACM model, term premium accounts for around 1.5%.

That leaves a true real yield of approximately 0.4%.

That’s an important number because despite the headline 4.3% yield that seems attractive, the economy is offering almost nothing in genuine real returns.

But what the breakdown really shows us is that despite inflation expectations falling from 3% four years ago to 2.4%, the differential of 0.6% has been more than made up for in term premium. And what that means is that the bulk of “new” compensation bondholders have been demanding is compensation for uncertainty and risk, not productivity and price increases. This build up in uncertainty premium is even more pronounced at the 20-year duration.

The question worth asking now is not why yields are high despite inflation having decreased substantially over the past couple of years since the COVID reopening, it’s why the uncertainty premium has come back so strongly after eight years of near-zero. And that requires a discussion on term premia.

The return of the term premium

First of all, what is a term premium? In plain terms, it’s the extra compensation investors demand for holding long-duration bonds over short term paper.

For much of the past decade, the term premium was effectively compressed out of the system, and in some periods it even turned negative.

This compression was a function of, you guessed it, quantitative easing and monetary debasement, as well as strong global demand for safe assets, low and stable inflation, and high confidence in central bank frameworks/stimulus.

In that environment, long-term yields were largely a reflection of expected policy rates, not risk. Risk in any meaningful sense was not being priced. You could see that in the tiny spreads between corporate and government bonds, as well as the huge valuation multiple expansion in equities markets.

But that regime has now changed, and the term premium has re-emerged as a genuine component of long-end yields.

As the chart below demonstrates, investors are once again demanding compensation for holding an asset with a longer duration. Not just for time, but for uncertainty.

That means risk is once again being priced—value investors are rejoicing.

Inflation is stable. Uncertainty is not.

Mathematics aside, the sniff test is that if inflation expectations were the primary driver of higher long-end of the curve yields, we would expect to see a much sharper move in break evens, but we have not.

In fact, as the chart below shows, inflation expectations have been range bound since the second half of 2022.

What has shifted instead, is the range of possible outcomes around inflation, policy, and fiscal settings.

That distinction is critical. Markets are no longer pricing a single, stable path. They are pricing a distribution due to uncertainty.

And when that distribution widens, the required return for holding long-duration assets rises with it. That’s the key point.

What is driving this re-pricing of risk?

Several forces are now feeding this re-emerging term premium.

Persistent fiscal deficits and elevated government bond issuance to finance them means that investors must absorb significantly more duration risk, and that alone places upward pressure on long-end yields.

Meanwhile, even if the central case for U.S. inflation sits near 2% to 2.5%, the path is less predictable than it was. We will see CPI prints rise from higher prices resulting from Hormuz oil, fertiliser and food impacts, but how long that will last is an open question. The fact remains that so far, the “new” build-up in long term yields is mostly term premium.

Volatility, not just level, is now being priced. And the reactionary function of central banks has also become more complex than it was pre-COVID, leaving markets with less confidence in a smooth, predictable policy path.

Layered on top is a broader geopolitical and policy overlay. The influence of Donald Trump is best understood in this context. Of particular note is his favoured use of weaponised tariffs, a more fluid geopolitical stance, a wider range of potential policy outcomes, and more coordination between the Bessent-led Treasury and the Fed, which I’ve written about extensively in my work on TIFFIT and the QE Infinity Train to Nowhere.

These drivers have enabled an environment where uncertainty is harder to bound, hence a wider distribution of outcomes is bringing term premia almost back to where they were last century!

A shift in how markets price the long end

The implication is straightforward, but underappreciated.

For most of the last decade, long-term yields were essentially a proxy for (and response by bond vigilantes to) expected policy rates.

Today, they carry a meaningful additional risk premium on top of that, which is a fundamentally different market structure and carries real consequences.

Even if inflation moderates or policy rates stabilise, term premia can keep long yields higher than the rate path alone would imply, which is to say that a steepening curve is no longer just a signal of rate cuts ahead, it reflects rising risk premia instead.

What this means for corporate development, M&A and investments

Higher term premia, not just at the extreme long end but at the 10-year duration feeds directly into the capital asset pricing model (CAPM) which calculates a firms’ cost of equity. When blended with the cost of debt, this determines the weighted average cost of capital which is then used to discount forward cash flows and calculate business and financial asset values.

As the cost of capital increases, so does the discount rate applied to future cashflows, pushing down an assets’ present value. This means trying to raise capital at the “old valuation” becomes heroic as the term premium increases, which is what’s happening now. As valuations decrease, financing conditions become tighter and greenfield projects become more challenging to finance because funders and investors demand more compensation as project risk duration increases.

Aside from critical minerals and AI-oriented capex projects, the re-emergence of the term premium is another reason why M&A is likely to remain the preferred corporate development tool for longer.

It also means increased interest in non-traditional bridge, royalty, stream, offtake prepayment, and sovereign fund financing methods, as we are now seeing.

What the compressing term premium meant for the 60/40 portfolio. And why it broke.

The compression era was not just an academic curiosity. It was the engine behind one of the most reliable portfolio constructs of the past three decades.

Through the 2010s, as term premium fell and bond yields declined steadily, long-duration bonds offered something close to a structural free lunch. When equity markets wobbled bond prices rose, delivering capital gains precisely when investors needed them most. The negative correlation between equities and bonds was not just holding. It was being amplified by the ongoing tailwind of falling yields. The 60/40 portfolio worked exceptionally well in that environment, and for good reason.

And like everything else that’s good until it’s not, that relationship broke in 2022 and hasn’t fully recovered. The unwind of the curve inversion has been painful for bondholders, to say the least. While short-end yields were attractive on paper, anyone reaching for duration has faced capital losses as long yields have ground higher. TLT, the iShares 20+ Year Treasury ETF and the most common vehicle for long-duration exposure, closed at $86.28 on 16 April 2026. It hasn’t been investable for a few years because yields are still rising, with a large part of the reason being inflation expectations and the term premium.

And the reason for this is precisely what this article describes. Term premium is still being re-priced upwards. We have not yet seen a clear ceiling. Until that repricing runs its course and a top is established, duration remains a speculative call rather than a defensive one. 60/40 hasn’t been working since COVID.

When the term premium does find its level and fiscal trajectories become clearer, policy uncertainty recedes, and investors feel adequately compensated for the risks they are taking, long bonds will become viable again. TLT will have its moment. But that moment requires patience, and possibly more pain first.

The bottom line for corporate developers and investors

Inflation explains part of the story but doesn’t explain the shift. The U.S. Treasuries market is no longer just pricing where rates will go. It’s pricing how uncertain the path has become. And given the Eurodollar market favours Treasuries as its number one form of collateral, yields in all countries are influenced by it.

So, after more than a decade of suppression, risk has returned to the long end of the curve. The cost of global finance has risen, and asset valuations are under pressure. Risk rarely disappears quietly once it returns.

Here’s where I think we are going.

CorpDev/Growth strategy: Expect more M&A and less greenfield development. Key exceptions will be in geopolitically driven projects in energy, critical minerals, precious metals, sovereign capability, AI data centres and related capex.

Early-stage capital: More than 70 cents in every US VC seed dollar (per Carta 2026 data) are now going into AI. Australia rhymes with this, although origination is led by family offices and high-net-worth investors, not VC. Nonetheless, if your investment thesis sits outside AI infrastructure or the application layer, your pricing must reflect that. The alternative is to wait for a future window once the 10-year yield falls. Which strategy is better for you?

Corporate debt: Especially here in Australia where another policy rate hike is squarely on the table, expect corporates to offer more term premium on longer-duration issuance. Will investment-grade fixed rate bonds approach 7% this year?

Investors: If investment grade fixed rate corporate bonds hit, or approach 7% this year, odds are on for a rotation out of Australian equities, perhaps other than for certain materials (precious metals, rare earth, critical minerals). Few analysts are talking about this scenario, preferring to focus on how to trade news from the Strait of Hormuz.

To finish today’s article, bond markets are pricing both inflation and risk within a wider distribution of outcomes—call it an uncertainty premium that increases the longer the investment duration is. The term premium is back, for the moment.

For my Australian business owner/project developer readers, ensure your financing and growth strategies align with higher Australian rates for longer and the continuing geopolitical focus on defence, critical minerals, DCs, and sovereign capability manufacturing.

For Australian investors, one eye on Hormuz is wise, but perhaps consider what might happen if there is a rotation out of equities if long-duration investment grade fixed income yields approach the 7% plimsoll.

See you in the market 🖐

Mike

With decades of success across six continents, NextLevelCorporate helps you navigate the intersection of M&A, financial advisory, and business strategy —delivering macro-aligned corporate development strategies and the transactions that bring them to life.

All content is copyright NextLevelCorporate. NextLevelCorporate and logo are registered trademarks.