When slowing prices can be good and bad at the same time

Image: jiří mikoláš

Living here in Australia, which is highly exposed to the USD, it’s important to keep up with goings on in the home of the brave and land of the free.

Recently, there have been three key lagging indicators pointing to a slowdown in the U.S. economy.

1. Manufacturing PMI was down in October.

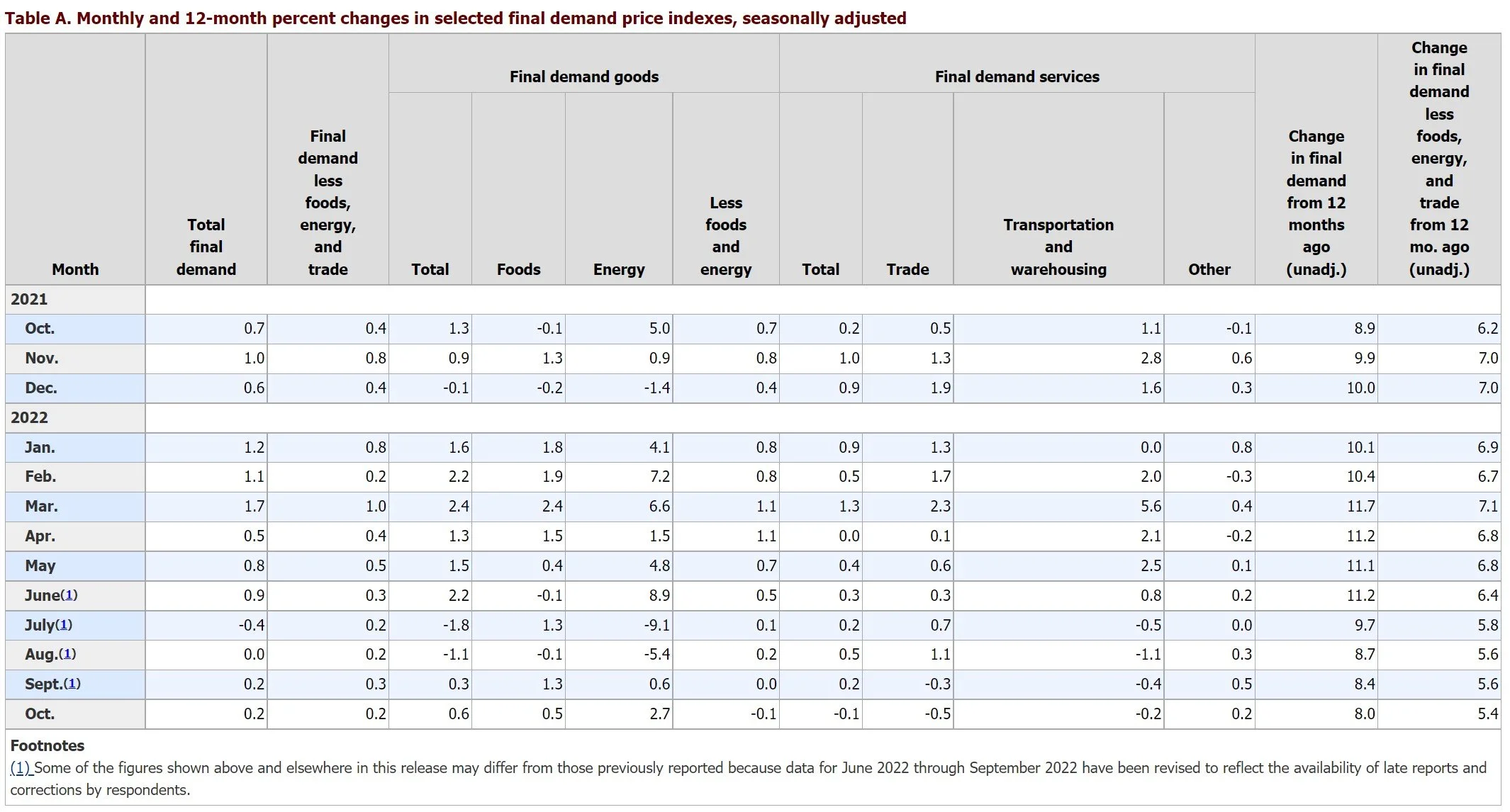

2. CPI was way below what was expected in October, printing 7.7% year on year.

3. Yesterday, the PPI or producer price index, printed a level that was lower than what most economists were expecting, coming in at 8% year on year and around 26% down from its highs during the Russian attack on Ukraine.

Then there is a key leading indicator, the bond market. Bonds seem to be in agreement with the lagging indicators.

That is, the 2-year treasury has rolled over to where it was at the end of September. It’s down 40 bps, and similar in move to the 10-year treasury meaning bond prices are rallying.

But bonds, which are forward looking, might be saying something very different.

There are two camps.

The first camp thinks bonds are simply factoring in slowing inflation, and in turn falling expectations for more aggressive interest rate hikes. This is the obvious one and consistent with equities rallying on sentiment. But it’s probably a premature reaction (again) given Fed Chair Powell’s guidance. Most of all, it is backwards looking - yet the bond market does not look back, it looks forward. Peeps in this camp are equity bulls, bond bears, and busy ‘willing up’ equities and crypto.

The second camp is probably smaller. Peeps in camp 2 say Powell will continue to go hard, but that his strategy is a mistake (like 1928/29) and that what we are really seeing is the bond market starting to recalibrate its expectations for aggregate demand/real growth (not just inflation). That is, the Fed has already overtightened (in the worrying face of 4x global debt to GDP) and the effect on aggregate demand is likely to be profound. These people are equity bears, selling out on dead cat bounces (if not already out of equities and crypto) and some are short…

…and I mean very short.

Attribution: prompted by Bruce H and Mike G in amusing discourse on Burry, SB-F and other signs of an incoming short…….…..

Which camp are you in?

Are you expecting a Lehman moment (out of FTX or some other failure yet to show itself) or do you think it will be a slow grind sideways until sentiment changes, or are you still partying till you puke, Bruh?

Mike

Image: Hygor Sakai

Next Level Corporate Advisory is a leading M&A and capital markets advisor with a 20 year track record of delivering the highest quality of independent financial advice as well as strategic transactions to help companies of all sizes level-up, in and out of Australia.

All text in this article is copyright NextLevelCorporate.