No Pivot, No Panic—what Fedopause means for Dealmakers and Investors

© nextlevelcorporate, 2025

TL: DR

The Fed is unlikely to hit its 2% inflation target any time soon.

Rate cuts are less likely than markets hope.

Tariffs and supply-side pressures are keeping prices sticky—hence the ‘Fedopause’.

Cost of capital remains high; and ‘revenue risk’ gauges flash red as many geopolitically critical projects require sovereign support just to be viable.

For companies, corporate development currently favours M&A over greenfield risk when it comes to geopolitically sensitive non-terminal metal projects.

For investors, the resumption of a weakening USD (following the ceasefire) will again unlock pockets of global liquidity, presenting cyclical investment opportunities outside the U.S. Risk markets know this. Risk-on.

On the flip side, if Hormuz lights up and oil ticks up again, the dollar will strengthen, liquidity will recede (all other things being equal) and risk assets may pull back.

U.S. monetary policy update

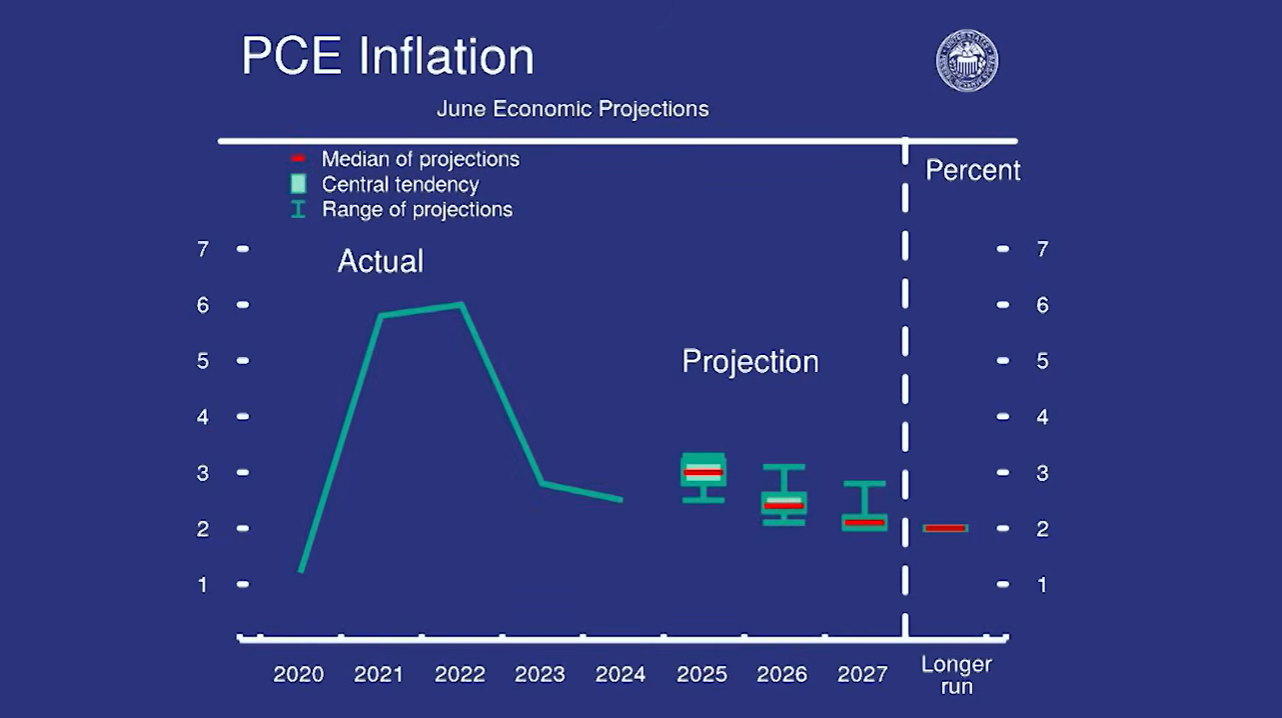

The Fed wants core PCE inflation to be sustainably brought down to 2%.

Remember, central banks base decisions on historical (not forward looking indicators like Truflation).

Well, we’re still miles away from target.

And the problem for deflationists is that as of last week, and not in the least due to tariff effects, the Fed’s June Economic Projections indicate it expects inflation to be 3% by year-end, not 2%. That’s 50% above target.

The Federal Reserve Board

As for interest rates, the median projection is 3.9% by year-end.

With the current Federal Funds Rate (FFR) sitting between 4.25% and 4.5%, the dot plot is implying two 25 basis point rate cuts.

But if tariffs keep lifting prices, even those two cuts might not happen.

And there are a number of Governors who believe the FFR will remain above 3% well into 2026.

So, higher rates for longer (still) seems like the highest probability at this time.

The bond market agrees. At the time of writing, the 10-year Treasury yield (essentially the risk-free rate) was sitting at 4.38%, right in the middle of the FFR range. Meanwhile, the 2-month Treasury yield jumped to 4.58%, indicating the curve is inverted on expectations of short-term inflation pressure.

On that point, I posted last week on LinkedIn that the upswing in the Import Price Index (excluding food and fuel) could give the Fed cover to hold firm. And it did.

As a quick refresher, the month of May saw meaningful price acceleration across several import categories 👇👇👇

U.S. Bureau of Labour Statistics

That release landed the morning of the FOMC meeting. One suspects Trump’s camp wasn’t thrilled 🤮.

But with high prices, historically low unemployment, and the labour market still pulling in 35% more people per month above the neutral employment watermark, there’s no market-based reason for the Fed to cut.

If Treasury issuance stays brisk and buyers remain, there’s yet another reason rates are unlikely to budge.

So:

No pivot.

No guarantee of two cuts.

No real-world pressure to ease monetary policy—no matter how much political noise surrounds the Fed Chair (or the Don’s efforts to campaign for a seat on the board).

While unemployment stays anchored, it’s a Fedopause until sticky inflation is no longer sticky.

Essentially, the Fed’s “gone fishing” until further notice.

What now?

🧱 Corporate development strategy

For corporate development, the cost of capital and WACC remain high. That environment favours:

M&A over greenfield risk.

Projects with demonstrable margin and resilience.

Caution when assessing geopolitically sensitive projects propped up by government intervention, especially those driven by "strategic" product shortages.

Supply chains are still shifting, balancing margin protection with tariff management, sovereign capability, and geopolitical realities.

💰 Investment strategy

Despite the absence of a cut last week, there was talk of a possible July cut, which equities markets took as a dovish signal (regardless of what the bond market is saying).

Cyclically, the USD continues to weaken (‘going Kenobi’), injecting liquidity into non-U.S. economies. For many, it now costs less to access USD in the Eurodollar market. That helps ease import costs and improves purchasing power.

What could go wrong with that? Well, first of all, if Hormuz arcs up again (despite current ceasefire indications) and oil ticks above a Bradman, the dollar will strengthen. And while long duration tech stocks and anti-debasement assets like bitcoin and gold will continue to do well long term, there could be some cyclical weakness under a higher oil/higher dollar/lower liquidity scenario—if it were to happen.

Secondly, watch for noise versus signal when it comes to Trump tactics versus long term strategy.

If you’re dealmaking or investing—make sure you have one ear tuned to the macro, and the other tuned to geopolitical strategy (not tactics, which are typically short-lived).

Mike

The Fed’s in a bind until it can see inflation (measured historically) sustainably returning to 2%

With decades of success across six continents, NextLevelCorporate expertly navigates the intersection of M&A, financial advisory, and business strategy—delivering macroeconomically aligned corporate development strategies, with bespoke transactions that bring them to life.

All content is copyright NextLevelCorporate. NextLevelCorporate and logo are registered trademarks.