RBA surprised as inflation didn’t glide lower — it re-inflated

Joining the data centre boom. (c) NextLevelCorporate, 2026. All rights reserved.

TL; DR

Yesterday’s speech from Michael Plumb of the Reserve Bank of Australia (RBA) was meant to be a scene-setter. Instead, it confirmed something more consequential: the disinflation story many were getting comfortable with in mid-2025 has stalled. Sound familiar?

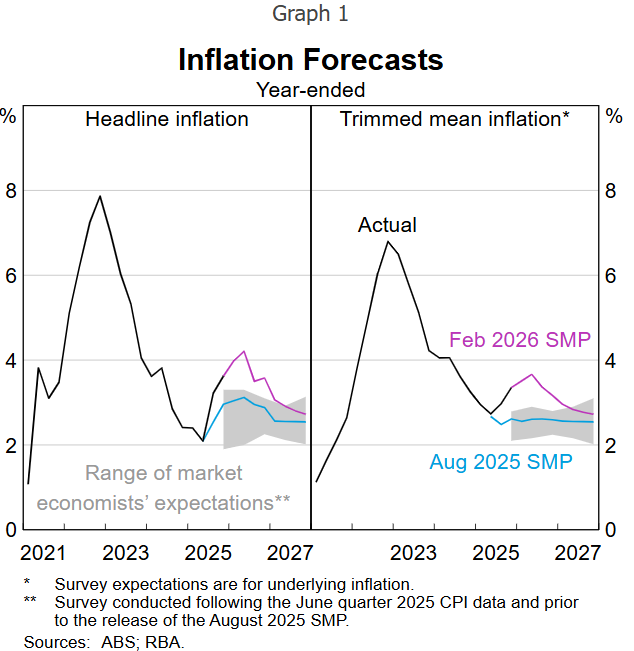

Of course it does. Underlying inflation was expected by the RBA to drift toward the midpoint of the banks 2–3% target band. Instead, there was a marked increase in inflation in the second half of 2025.

Over the year to the December quarter, headline inflation was 3.6% while underlying (trimmed mean) inflation was 3.4%, meaning inflation re-accelerated by the December quarter with price pressures broadening materially across the basket.

Source: RBA, Recent Developments in Inflation and the Economic Outlook, 24 February 2026

The key takeaway is not simply that inflation rose. It’s that the RBA underestimated both the breadth of the move and the persistence of demand. Declining productivity and data centre formation for construction.

This morning, the ABS released the annual CPI print to January.

3.8%.

This shifts the policy balance. For Australia, a lot now rests on whether this wave of data centre and energy investment delivers genuine productivity gains — fast enough to offset the inflation it is currently helping to create alongside the government’s other spending proclivities.

The easy explanation turns on volatile sector-specific pressures

Part of the story is mechanical. Travel and fuel rose. Electricity rebates unwound. Homebuilders and retailers stopped discounting as demand firmed. Many commentators had warned about these elements.

In 2024 and early 2025, discounting suppressed measured inflation. In the second half of 2025, that effect reversed.

When promotions disappear, the CPI lifts, even if the underlying cost base hasn’t structurally changed.

The RBA believes much of this will dissipate. But that’s only part of the picture.

The harder explanation is demand was stronger than anyone thought

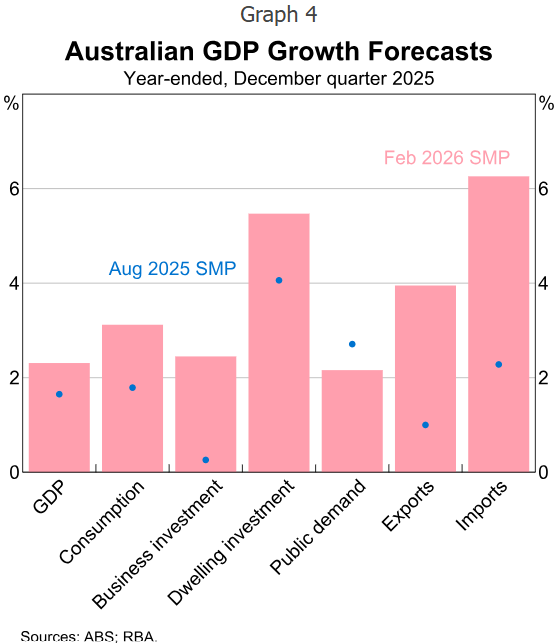

The more important driver is aggregate demand. GDP nowcasting this February were raised well above the calls made in August, in all categories of private demand.

Source: RBA, Recent Developments in Inflation and the Economic Outlook, 24 February 2026

While the RBA won’t receive the December quarter national accounts until next week, its latest nowcast (the pink columns in Graph 4) is that GDP growth over the second half of 2025 was “a little above” their estimate of potential growth, and higher than the RBA had expected in August.

I assume that’s a reference to the first column, only? Because the bank totally missed on all constituent parts. And it doesn’t seem to be a statistical quirk. Several forces converged in the nowcasting:

Global resilience. The feared external shock did not materialise. Tariff impacts were diluted by TACO exemptions and supply chain reconfiguration, including bring-forward expenditures.

Financial conditions were looser than assumed. Credit growth was robust. Risk premia remained compressed.

Households were stronger. Real incomes improved. Wealth effects still supported consumption.

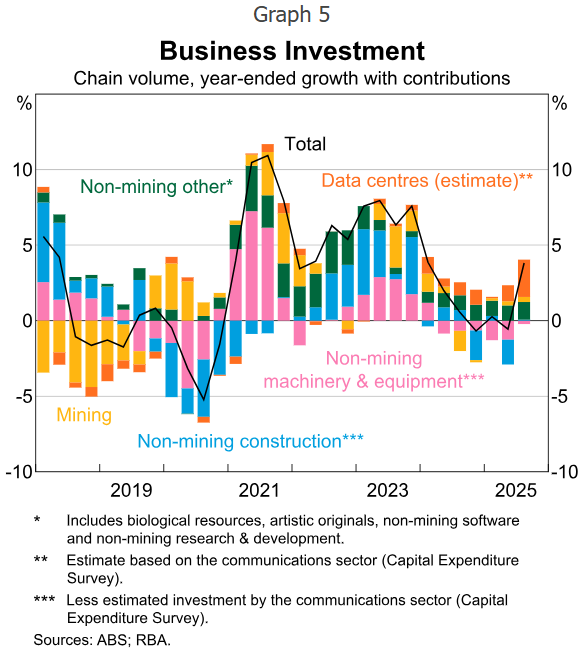

Business investment surged. Data centres and compute/intelligence capex was not limited to just the U.S.

And this is where it gets really interesting.

The Orange Crush of data centres and the new capex cycle

The standout in business investment was data centre fitouts.

Source: RBA, Recent Developments in Inflation and the Economic Outlook, 24 February 2026

Those orange bars are the story and the signal, which is to say that a material share of the September quarter capex surge came from data centre buildouts. This was largely imported equipment, lumpy by nature, and directly tied to AI and cloud infrastructure expansion. At the time, the AUD was only buying 65-67 U.S. cents, making those lumpy purchases more expensive than they would be now, at around 71c to one AUD.

The RBA expects the magnitude to moderate. But the broader theme remains intact.

Firms have upgraded investment plans in utilities, energy, technology and non-residential construction.

This is not a local anomaly. It mirrors what we’re seeing in the U.S., where some fear that if the downstream AI monetisation layer does not monetise, the upstream picks and shovels will start to weaken.

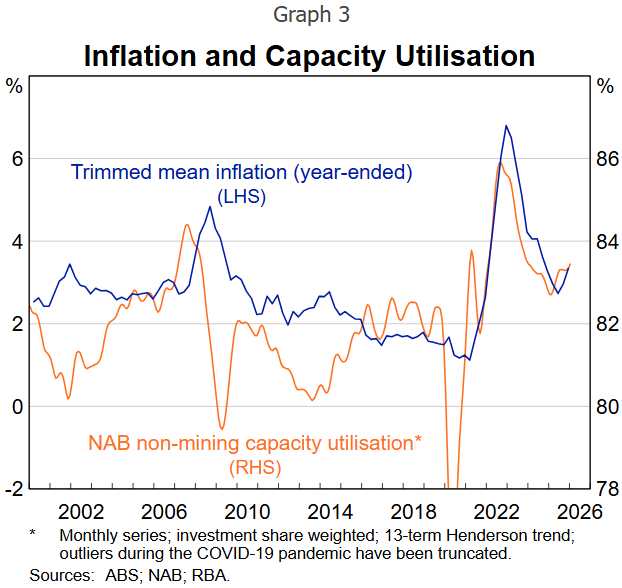

Capacity isn’t just about demand, it’s about supply limits

The RBA also revised down its estimate of supply capacity.

Unit labour costs remain elevated. Business surveys show higher capacity utilisation. Labour constraints are persistent.

Source: RBA, Recent Developments in Inflation and the Economic Outlook, 24 February 2026

The uncomfortable possibility is that potential growth is lower than previously assumed, partly because productivity remains weak.

When demand surprises on the upside and supply disappoints at the same time, inflation doesn’t glide back to target. It embeds. We saw that in 2022 due to more extreme supply shocks from lockdowns.

The policy implication is higher rates for longer in Australia

I feel like a broken record on this point. It’s a reason why markets grind sideways each time an inconvenient inflation print comes out. This time, the February forecasts assume a higher path for the cash rate than was embedded mid-2025. Inflation is now expected to peak mid-2026 and only gradually return toward the midpoint by 2028.

That is not a quick re-normalisation story. That is not transitory. That is a result of high non-tradable inflation and a heavy spending government policy.

Even if sector-specific pressures fade, broader capacity tightness for lack of productivity (and a high- cost energy, labour and housing base) means the RBA cannot ease prematurely without risking credibility.

The balance of probabilities now leans toward interest rates remaining in restrictive territory for longer. And that’s:

Good news for importers, savers and fixed income.

Not so good news for marginal borrowers and those waiting for a pivot to light up equities and crypto.

Uncertain yet familiar times for exporters since higher interest rates support a higher dollar relative to the U.S., leading to less return in AUD, but potentially higher volumes of more affordable commodities sold.

Overlaying the U.S., why a global cutting cycle may be delayed

In the U.S., the narrative is similar but amplified.

Growth remains firm and heavily driven by AI-related capex and energy infrastructure. That growth and other reasons make it harder for the Federal Reserve to cut aggressively, at least this side of the June FOMC meeting.

Trump Tariff policy (non-legal and legal) remains fluid, but the critical point is that when capex is strong and labour markets remain tight, central banks hesitate to ease.

Even Fed Governor Chris Waller said the other day that it might be appropriate to keep rates steady if labour market data for February indicates downside risks to the labour market have diminished,

If the U.S. holds rates higher for longer, Australia can’t drift too far in the opposite direction without currency consequences.

If it did, one of the consequences would be a weaker AUD against the USD, making imports more expensive. In the absence of government intervention, this would not be a good outcome if imports continue to grow at three times the rate expected by the RBA (refer Graph 4).

The bigger bet, the global data centre and energy super cycle

The data centre capex boom is not cyclical noise. It is global signal.

AI, cloud computing and digital infrastructure require enormous compute capacity. Compute requires power. Reliable power requires dependable energy infrastructure, i.e., reliable generation, transmission and storage.

This creates two realities:

Productivity gains are heavily contingent on successful deployment.

Energy must be abundant, stable and scalable (with sustainable in fourth place).

That runs into tension with parts of the green transition narrative that assume rapid decarbonisation without materially expanding dispatchable capacity.

If energy supply fails to keep pace, inflationary pressure migrates from wages to electricity and industrial inputs. In short, the AI, automation and robotic build-out is deflationary only if energy supply expands fast enough. Otherwise, it is inflationary.

Read that again 👆

What it means for Australia, corpdev and investing

For Australia, this environment has layered implications:

Higher rates for longer increases funding discipline.

Global capex strength for compute and defence supports demand for industrial inputs.

Energy infrastructure expansion underpins commodities tied to electrification and grid build-out.

Currency debasement from impending increases in broad money due to persistently growing debts and deficits supports strategic allocation to precious metals and scarce commodities.

For corporate development, this means:

Projects tied to structural demand (energy, grid, data infrastructure) command premium strategic value.

Productivity improvements are essential, not optional, if margins are to be protected in a higher cost world.

Capital discipline matters more than narrative.

In the absence of productivity and also due to the cost of capital, a resurgence in M&A activity.

For personal investors:

Duration risk remains real and it is not being properly compensated.

Cash flow quality and value matters.

Picks and shovers upstream of compute are still underappreciated.

Precious metals continue to have a big role to play.

Defence has become a secular theme with strong tailwinds.

Commodity exposure should be strategic, not speculative.

Final thoughts

The RBA did not intend to signal alarm, nor poke the Treasurer, perhaps.

But the message is clear. Inflation’s descent has stalled because demand was stronger and capacity thinner than assumed.

Overlay that with a global geopolitical buildout in AI, chips, data centres, energy, critical minerals and defence, and the “higher for longer” regime look less like a transitory posture and more like the base case — both for internal affordability and wealth effect, as well as external foreign exchange issues.

For Australia, a lot now rests on whether this wave of data centre and energy investment delivers genuine productivity gains, fast enough to offset the inflation it is currently helping to create alongside governmental spending proclivities.

See you in the market 🖐

With decades of success across six continents, NextLevelCorporate expertly navigates the intersection of M&A, financial advisory, and business strategy—delivering macroeconomically aligned corporate development strategies, with bespoke transactions that bring them to life.

All content is copyright NextLevelCorporate. NextLevelCorporate and logo are registered trademarks.