Metals Roundup Feb'26: bulls exited left, bears stormed the vodka

“It was their turn to party” Copyright, nextlevelcorporate, 2026.

Summary for February 2026

As I said last month, the bullish suds party the bulls enjoyed in January was poured from a keg of extreme risk-on sentiment. Bulk mineral and base metal prices accelerated at their fastest pace for years.

But it didn’t last long.

On 30 January, the Fed declined to cut the Federal Funds Rate and remained on pause, the December PPE surprised many people who didn’t believe inflation comes in waves, and Donald Trump announced Kevin Warsh as his Fed Chair nominee.

Markets (over)reacted violently, belting down stock prices and the bloodbath doubled down four days later after Anthropic announced its AI legal/professional services plug-in, signalling AI’s existential threat to cloud software was no longer existential.

And in February? All five base metals and bulk minerals bulls left the pub while the bears took their place. But instead of premium craft suds. the bears opted for the cheap vodka.

More recently, oil shortages resulting from the effective choking of the Strait of Hormuz have already resulted in higher oil prices and/or unplanned shortages (including here) and given the world is still addicted to petroleum products, this will eventually show up in the inflation numbers.

It’s also fair to say that when things return to normal, whenever that will be, there will still be pressure on fuel prices as G7 countries with depleting/depleted oil reserves seek to restock their strategic oil reserves, at the same time as shuttered producers recalibrate.

And that is what’s already putting upwards pressure on the USD and will further curtail commodity prices. It pays to remember that a strong dollar usually withdraws liquidity from markets outside the U.S., materially affecting affordability of imports in those countries and curtailing investment and consumption.

For these reasons, we are not at this time expecting a directional reversal in industrial metal prices in March.

If the war continues (despite Trump’s recent comment that “the war is very complete, pretty much”) and/or escalates, we are in for more oil, fertiliser and soft commodity shortages, resulting in price accelerations, sharp drops in demand for industrial metals, and a sharp regime change in risk markets, not unlike the 1970s.

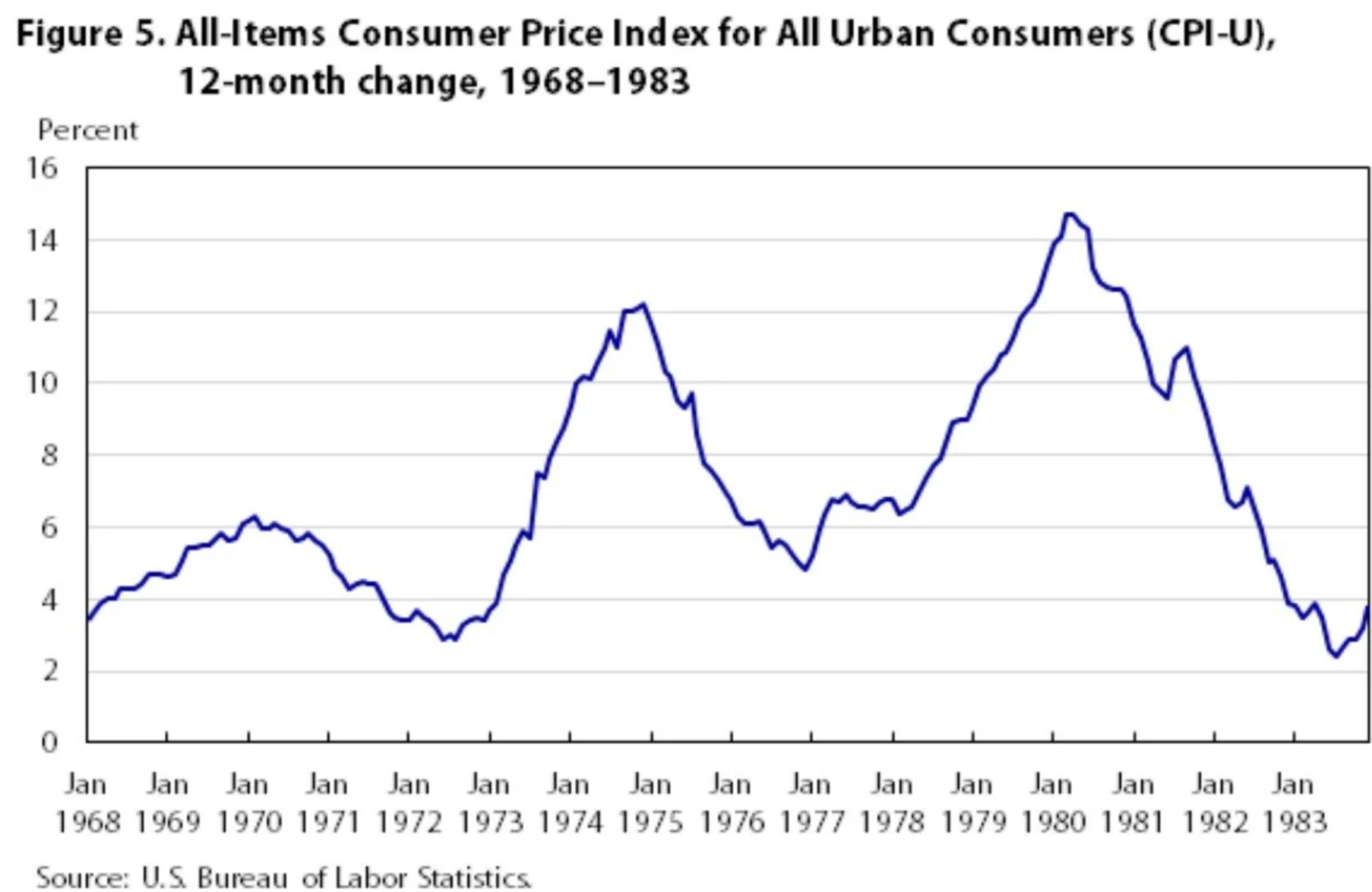

It’s beginning to feel a lot like the 70s, or is it?

In the 1970s, there were three oil price shocks which preceded three waves of inflation.

The first oil shock was caused by the 1973 Arab Israeli war.

The second came from the OPEC oil embargo in 1973.

The third followed the Iranian Revolution in 1979 when then Shah of Iran, Ayatollah Khomeini, seized power to become the first supreme leader.

Here’s what those wars and shocks did to consumer prices 👇

They all caused prices to accelerate at between 4 and 5 times the long-term average

I was in primary school at the time, but I remember well the Iranian images on our black & white TV, as well as the constant comments about high prices and inflation after a barrel of oil doubled in price (like it did last week).

The images from Iran over the last weeks have been eerily similar and just as disturbing.

Back in Australia in 1979, CPI ranged from 9% to 13% before peaking at ~18% in 1980. Unemployment hit 6% and change. And the level of pain can be seen in the steepness of those curves (i.e., the rate of change).

But as we say, history doesn’t usually repeat, but it does often rhyme, and each subsequent time can be a little different depending on the other factors at play.

If Trump and the new supreme leader are both done, we get a spike that shows up in some historical measure, sometime in the future, and then back to normal. If either one of them is not done, we get a whole lot of something else that won’t look nearly as good.

With that said, on with the charts!

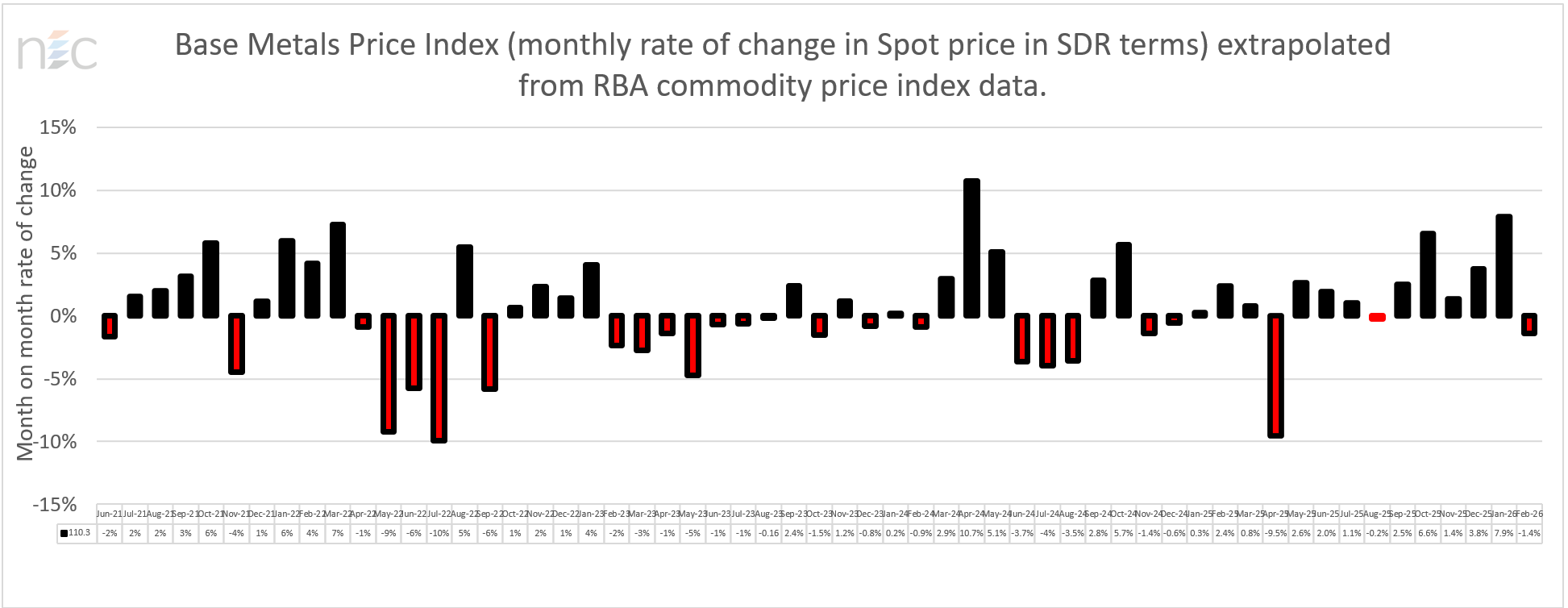

Your rate of change charts for February 2026

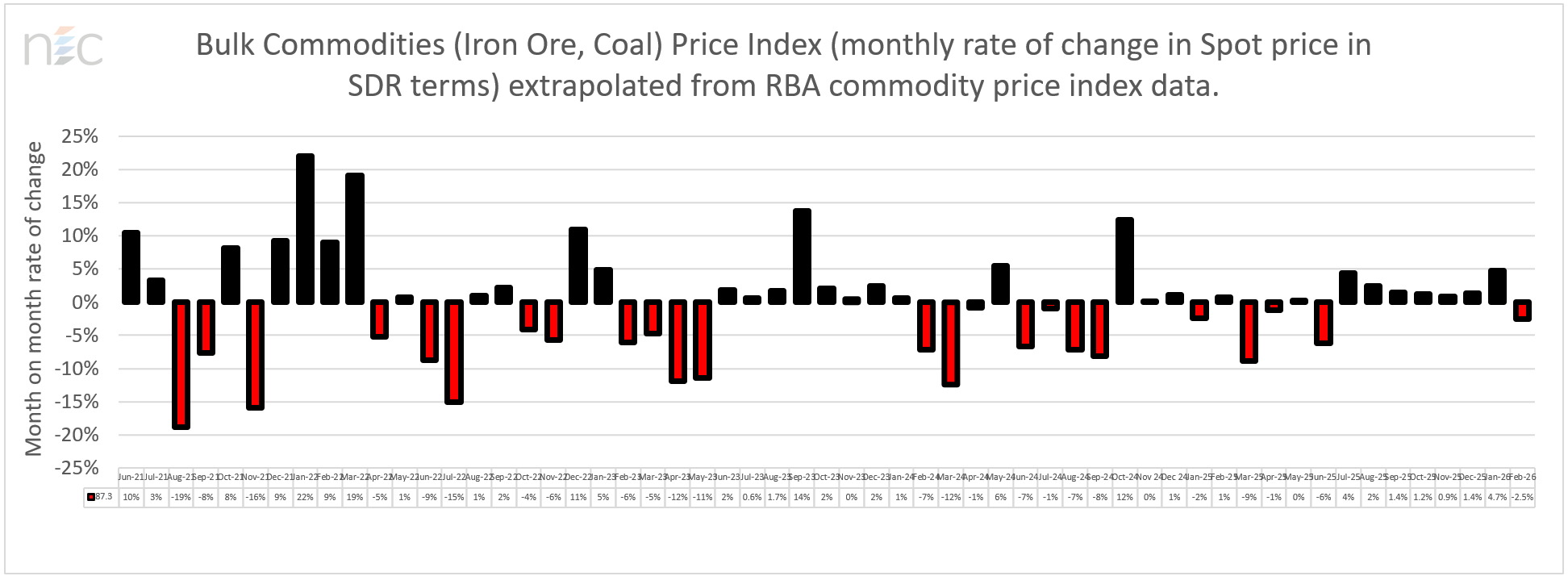

And here are your price deceleration charts for February.

🔗🏮🔌 Base Metals reversal

Month on month, the base metals index (copper, aluminium, zinc, tin, etc.) decelerated at a rate of 1.4%, a major reversal on January’s month on month acceleration of 7.9% — which was the second fastest rate of change in 4.5 years.

It was a one-off.

Copyright, NextLevelCorporate Advisory

🧱👷♀️🌉 Bulk minerals

Same story, but a much larger 2.5% monthly deceleration, breaking a seven-month streak of price acceleration.

Copyright, NextLevelCorporate Advisory

⚗🧲☢ Energy minerals (ex-coal and oil)

The July 6, 2023, price high for LME Lithium Hydroxide CIF was US$46,046.

On the last LME trading day of January, it printed US$20,150/t, another remarkable improvement, nearly double the price from two months earlier, but still more than 56% down from its July 2023 peak.

But there’s new life in that white power!

Uranium was trading at US$85.95/lb on 26 February 2026, reflecting the re-rating in energy-hungry tech recipients. Why Australia refuses to jump on board with the rest of world and develop nuclear base load power remains at best, a missed opportunity.

Fossil fuels are now more than ever making a structural comeback as I’ve been suggesting. This is predominantly due to demand from data centre formation and the requirement to exploit every available calorific unit, particularly as supplies of Russian, Venezuelan and now Iranian oil, vacillate.

This month, and as a result of unresolved issues in the middle east, there may be pressure to “de-sanction” Russian oil.

🪔 Oil

Speaking of which, by the end of February, Brent Crude was trading at roughly US$66/barrel.

Just before Trump’s backflipping off-ramp comments on Monday, it was trading at US$108.73. and yesterday it was down to US$86.70 per barrel.

A wild ride to be sure, and it’s important because industry, mining and agriculture still runs on oil as does personal transportation and heating in the northern hemisphere. Many intermediate products and fertilisers are based on petroleum and natural gas substrates.

But this only becomes a problem if oil rises for an extended period of time.

Local impact from global forces

It’s unlikely we will see the start of a new commodities super cycle in the short-term.

Last month (and in the months before) I said that while we were seeing cyclical dollar weakness (which is positive for commodities demand), it may or may not be enough to kick start a new commodities super cycle.

My hesitation was that while the USD had cyclically weakened, global liquidity had been draining, and sustained demand from China was yet to be confirmed.

And on top of that temperance, we now have two additional forces at play.

First of all, recalibration of the world order as geopolitics takes over from demand and programmatic intelligence takes over from software products. Second, we have more kinetic wars occurring with unresolved issues in Ukraine and Iran, and as already illustrated above, war induced oil shocks have always been inflationary.

Implications for your corporate development strategy: Higher rates for longer in the U.S. and Australia are likely for at least the foreseeable future given inflationary pressures (now exacerbated in Australia by the rising costs of oil imports which account for 80% of our national fuel demand). Greenfield projects other than for precious metals and government subsidised/supported strategic minerals are even more unlikely to occur as a result of inflation expectations and expected higher rates and potentially declining margins. In its place, there will be more M&A and energy leadership. This should accelerate in 2026. Capital raising will be selective. Watch unemployment.

Implications for your personal investment strategy: Until recently, we had been experiencing a level of USD weakness. Last month I said global liquidity had been draining not building, and that precious metals had come off since 30 January and shortly may represent solid buying opportunities. The bottom is still not in and may not be in for high volatility assets. More to come. Not done yet. We wait.

Overall, the full effects of 30 January on liquidity and Treasury/Fed policy coordination as well as the unresolved issues in Iran are yet to be seen.

In the meantime? Hard commodities super cycle on pause, interest rate cuts on pause, USD strength for the moment, and plenty of volatility until further notice as we speed towards a new multipolar world order, with hardly enough calorific units to get us there safely.

See you in the market 🖐

Mike

With decades of success across six continents, NextLevelCorporate expertly navigates the intersection of M&A, financial advisory, and business strategy—delivering macroeconomically aligned corporate development strategies, with bespoke transactions that bring them to life.

All content is copyright NextLevelCorporate. NextLevelCorporate and logo are registered trademarks.