Metals Roundup April'26: Base Bulls and Bulk Bears

“Base metal bull grew while the bulks headed to bed” Copyright 2026. nextlevelcorporate. nextlevelcorporate prompts, AI generated image.

Summary for April 2026 — bases rocketed, while bulks shrunk

Last month we took a well-earned break and went fishing with a bunch of metal bears. We didn’t sink the boat, but we did sink plenty of cheap vodka.

And now we’re back to the reality of inflation, Trump, Iran, and the somewhat bizarre green tea party that Xi laid on for Putin.

I think these spell the beginning of Plaza II, which is to say a multi-sovereign currency agreement or accord, that in this case would see a weaker USD, the flow of more affordable commodities (resulting from a weaker USD) to sovereigns that need them (think China and Europe) and more attractive long-term Treasuries from the perspective of foreign buyers.

If I’m right, the commodities super cycle will resume one Plaza II is in place. And that’s just the beginning.

Today, let’s dig into the monthly rate of change charts to see what happened with industrial metals and minerals in April 2026.

Your rate of change charts for April 2026

First of all, remember that the RBA recently rebased the index on which our rate of change calculus is based. On 1 April 2026, the index was reweighed according to an average of export values in 2023/24 and 2024/25 (previously 2022/23 and 2023/24).

Also, last month we added a three-month moving average to our curve. This makes directional changes (e.g., broadly accelerating prices, versus broadly decelerating prices) easier to spot.

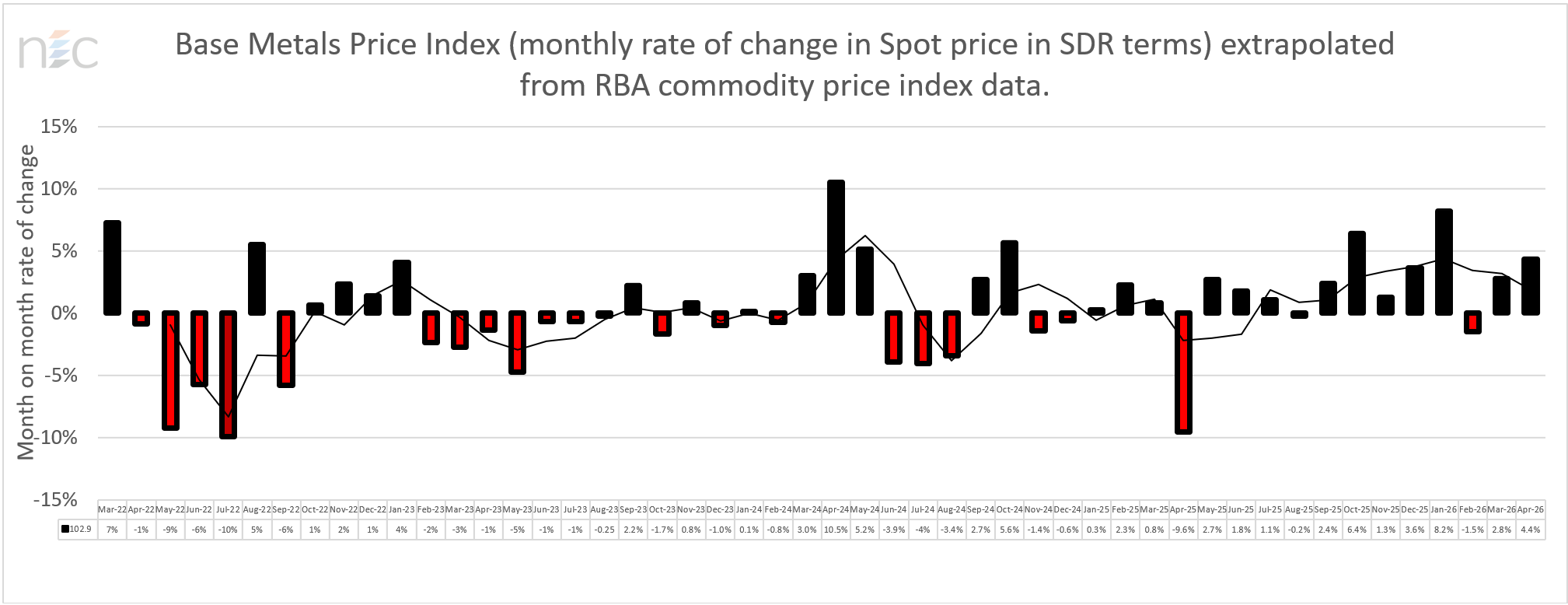

🔗🏮🔌 Base Metals follow through is April was the tell

Month on month, the base metals index (copper, aluminium, zinc, tin, etc.) accelerated at a modest clip of 2.8% in March, but the momentum continued into April with prices increasing at a month-on-month rate of 4.4%.

In other words, prices across the RBA’s base metals complex (e.g., copper, nickel, zinc, tin, etc.) grew at an even faster pace than the month before.

Base metals procurement for energy, electronics, manufacturing and other industrial uses continued to front run as the war in Iran showed no real signs of abating in April.

Whereas, from where we sit today, there are some signs that perhaps a form of Hormuz reopening (in a way, shape or form yet to be disclosed) might happen if the U.S. agrees to “park” the discussion on Iran’s nuclear program. Timing unknown. Human casualties unknown.

China, our largest export destination and trading partner, also showed signs of potentially having some influence over the outcome. Not quite the famous Nixon/Kissinger/Mao meeting in 1972, but conceptually not all that different given both the U.S. and China want something from each other and there is a quid pro quo to be had at the intersection of rare earths, Russia, Ukraine, food, oil, energy, chips, and Iran. Somethings to play for every sovereign that’s not asleep at the wheel.

We shall see a resolution when there is one.

Also note that since the end of April, LME copper, nickel and tin prices have come off after only one fortnight of gains. Hmmm?

Copyright, NextLevelCorporate Advisory

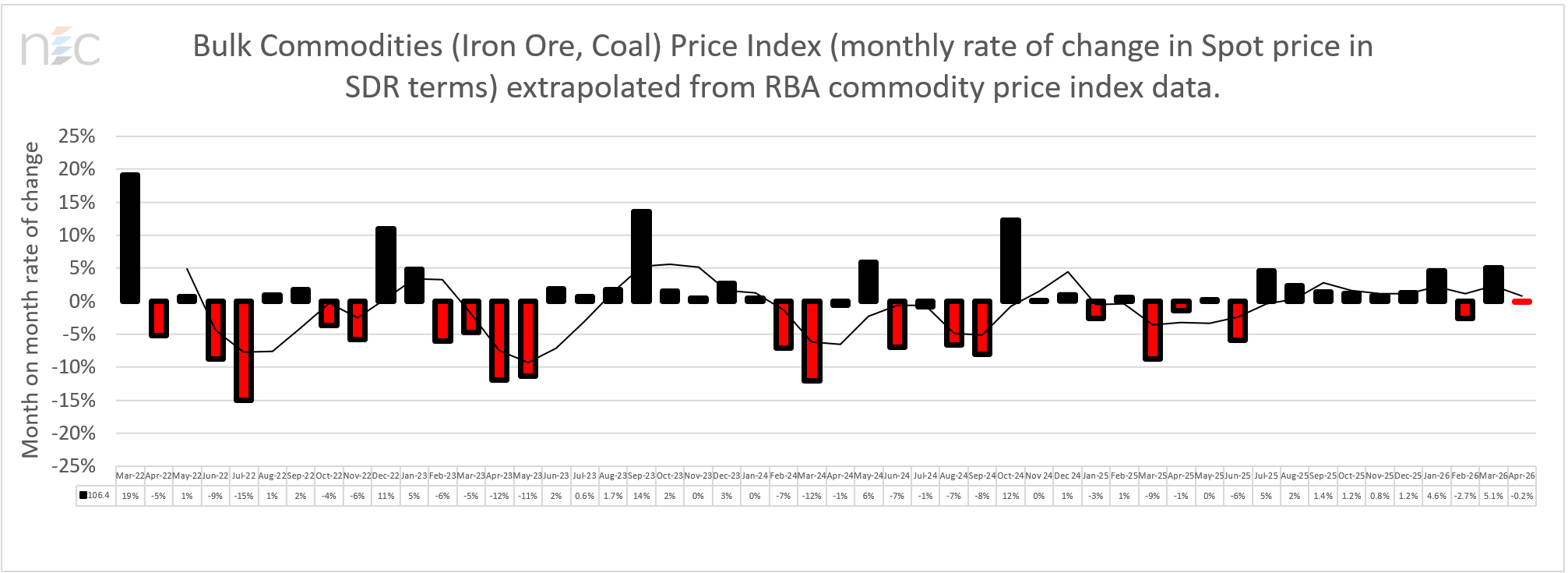

🧱👷♀️🌉 Bulk minerals

There was a massive about face in April. Bulk prices decelerated at a materially faster pace, and we now have negative growth and price decelerations in 4 of the past 12 months. The trend is slowing.

This makes sense because the Indonesia (and the U.S.) have been replacing some of our coal, with Indonesian coal and U.S. oil exports. And while steel is required to construct data centres, steel is plentiful whereas copper in particular is the real bottleneck for data centres and energy irrigation networks.

Copyright, NextLevelCorporate Advisory

⚗🧲☢ Energy minerals (ex-coal and oil)

The July 6, 2023, price high for LME Lithium Hydroxide CIF was US$46,046.

On the last LME trading day of April, it printed US$20,500/t, a small reversal (increase) since March, and still more than 56% down from its July 2023 peak. Petroleum supply shocks and shortages leading to some substitution/switching to EVs are what’s driving this.

But like rare earth prices, floors and geopolitical-driven support, what happens to lithium prices if there’s an accord under a Trump and Xi “kiss and make up” scenario?

Uranium was trading at US$86.80/lb on 30 April 2026, reflecting the re-rating in energy-hungry tech recipients. We expect uranium prices to continue “up to the right” although not in a straight line. But a $2 increase is a $2 increase. And uranium is not controlled by China.

Fossil fuels are now more than ever making a structural comeback as I’ve been suggesting. And as predicted last month, Russian oil was de-sanctioned and the U.S. is likely going to let China have more oil, for a strategic price, if we see a Plaza II accord.

🪔 Oil

To fade oil or not to fade oil. That is the question. It’s used in almost everything, and for our miners, the diesel price has a big say in operating margins for those who have not embraced a fully electric fleet, which is just about every miner, barring a handful.

On February 28, 2026, the United States and Israel launched coordinated airstrikes on Iran under Operation Epic Fury, targeting military facilities, nuclear sites, and leadership. The response was swift and economically devastating. Shipping traffic through the Strait of Hormuz virtually ground to a halt with a handful of vessel movements.

That narrow passage through which around a fifth of global oil production flows, and which also, as few people appreciate, transits around 45% of global sulphur exports needed in the production of fertiliser. Add to that Iran's missile attack on Qatar's Ras Laffan (the world's largest LNG liquefaction plant) causing extensive damage to Qatar Energy’s infrastructure, and halting ~330m m3 of LNG/day (20% of global trade) via the Strait. You can read more here.

We are still living inside that oil shock, and since the conflict began the price of crude oil jumped to above $100 per barrel on several occasions, up from around $67 before the first strikes. Mojtaba Khamenei has vowed to keep the Strait blocked as a tool of pressure, and Iranian military commanders have raised the spectre of oil at $200 a barrel. That pricing is looking unlikely from where we sit today, but things can change quickly particularly as second, third and fourth order effects of delays, missed planting seasons, rising food and fuel prices and shrinking business margins flow downstream.

At April month end, Brent crude and West Texas Intermediate were trading at ~US$110 and ~US$105 per barrel, respectively. Today, we are again under $100 and heading for $90.

Local impact from global forces

At the behavioural level, if the war continues, we may see a similar form of behaviour as manufacturers and constructors continue to buy material stocks in anticipation of disruptions. The “base effects” of that in the index will make it look like prices are accelerating.

At a macro level, global liquidity is rising moderately, with about $150 billion added in the U.S. alone since the end of April. This liquidity is mainly from fiscal spending through the TGA. This is inflationary.

At the same time, we’re still living through a messy recalibration of the world order as geopolitics takes over from demand and programmatic intelligence takes over from software products. This is inflationary.

Finally, we have more kinetic wars occurring with unresolved issues in Ukraine and Iran, and as already illustrated above, war induced oil shocks have always been inflationary.

And we are about to witness trillions of dollars of IPOs in the U.S. (SpaceX, OpenAI and Anthropic) which, if they all file and proceed, will create a wealth effect that will most likely take some steam out of second circle asset inflation and flip that pressure into third circle consumer prices. But they might also create so much dilution in the equities market that prices may just as easily come down. This level of IPO is unprecedented with some hedge funds positioning for a crash.

That said, this is what it all could mean for corporate development and investment strategies.

Corporate development strategy: I repeat our working thesis. Higher rates for longer in the U.S., and Australia are likely for at least the foreseeable future given inflationary pressures (now exacerbated in Australia by the rising costs of oil imports which account for 80% of our national fuel demand). At nextlevelcorporate we are seeing the effect of higher rates on several mineral projects that won’t be going ahead as a result of discounting at higher rates, inflated capex, and borderline debt serviceability. In its place, there will be more M&A leadership. This is accelerating. Capital is selective, but for favoured sectors, gold, rare earths and lithium, it’s strong. This can change quickly. Especially for metals that behave cyclically even though the long-term thesis is still intact. Watch unemployment from ageing demographics and AI substitution.

Investment strategy: The USD is not as strong as it has been during similar periods in history, probably because fewer oil barrels are transacting, petrodollar recycling flows are thinner, long U.S. Treasuries have been selling off, and capital is quietly finding other homes in response to Trump’s U.S.S Alonism which I have written about in client newsletters. For the moment, under this Administration, the wind is coming out of the petrodollar's sails. However, some green shoots in global liquidity are visible and if Hormuz reopens soon the market will likely look through the transition period. Are we in a bubble? Well, we should know not long after the SpaceX IPO. But equities capitulation and peak yields are still not in — we’re not done yet, so we wait.

Overall, the full effects of 30 January 2026 (the Kevin Warsh nomination and accelerating inflation) on liquidity and Treasury/Fed policy coordination as well as the war in Iran are working their way through financial and commodity markets.

While the USD is surprisingly weak given the circumstances, it may suddenly reprice. Kevin Warsh is the new Fed Chair and as a result we will start to see TIFFIT in full flight, which means the USD is likely to weaken and liquidity in markets is likely to grow. But it will take time.

In the meantime? Hard commodities super cycle on pause (but for frond-end loading of bases to avoid expected shortages), interest rate cuts on pause, and plenty of volatility until further notice as we speed towards a new multipolar world order, with hardly enough calorific units, transformers, and rail to get us there safely.

See you in the market 🖐

Mike

With decades of success across six continents, NextLevelCorporate expertly navigates the intersection of M&A, financial advisory, and business strategy—delivering macroeconomically aligned corporate development strategies, with bespoke transactions that bring them to life.

All content is copyright NextLevelCorporate. NextLevelCorporate and logo are registered trademarks.